In Toronto, construction starts on three- to five-unit small-plex buildings just surpassed 100-plus-unit projects for the first time on record. In Vancouver, Vancity announced on April 8, 2026 that its multiplex construction mortgage program — launched in Fall 2025 — has now financed 45 projects worth $60.4 million in approvals. Both numbers point at the same shift.

The Big Six banks don’t want sub-$5M multiplex deals. Credit unions are taking the entire category.

If you’re a homeowner trying to finance a four-plex on a Vancouver lot today, that’s the story you need to understand before you talk to your bank.

TL;DR (Key Takeaways)

- Toronto: small-plex (3–5 unit) construction starts have surpassed 100+ unit project starts for the first time on record

- Vancity has financed 45 multiplex projects ($60.4M) since its construction mortgage program launched Fall 2025

- Vancity’s expanded program offers up to 80% LTC, 18 months interest-only during construction, flexible co-owner amortizations, and rental offset for qualification

- The Big Six banks aren’t writing sub-$5M multiplex deals at scale — these projects are below their underwriting threshold

- Credit unions and alt-A lenders are filling the gap because Bill 44 created a structural pipeline of small deals the big banks don’t want

- Pre-sale-driven condo high-rises are stalling — financing has shifted toward smaller, faster-to-build, lower-density projects with rental income

- For Vancouver and Burnaby owners, the practical implication is start with credit unions, not banks

Two markets pulling apart

Canada’s residential construction market is splitting.

The high-rise condo side is stuck. Pre-sales are weak, construction costs are still high, and lenders that financed off-the-plan condos through 2022–2024 are pulling back. Projects that need 60–70% pre-sales to break ground are missing the threshold and going on hold. CMHC and BCREA forecasts have been signalling this since late 2025.

The missing middle side — multiplex, small purpose-built rental, three-to-five unit infill — is moving. Bill 44 unlocked the zoning across BC. Ontario’s Bill 23 and similar provincial moves did the same in major Ontario markets. The pipeline is real, but the deal sizes are small. A typical Vancouver R1-1 four-plex is a $3.5M–$5M project. A 100+ unit tower is a $50M–$200M project.

For a Big Six bank, those two deals require almost the same diligence work but produce wildly different revenue. The bank chooses the tower. Or, increasingly, neither.

That gap is where credit unions are now living.

What the Big Six want vs. what multiplex is

The Big Six (RBC, TD, BMO, Scotiabank, CIBC, National Bank) have multi-unit construction programs. On paper, a multiplex qualifies. In practice, three things make it a hard fit:

- Deal size. Most multiplex projects sit below the $5M–$10M threshold where bank credit teams can underwrite efficiently. The relationship manager doing a $4M four-plex earns the bank roughly the same revenue as a $40M mid-rise — same approval committee, same documentation, one-tenth the loan.

- Sponsor profile. Multiplex sponsors are often homeowners, family groups, or first-time small developers — not professional development companies with track records of completed mid-rise projects. The credit memo doesn’t write itself.

- Product type. Multiplex frequently sits in a grey zone between residential and commercial — too small for the commercial real estate desk, too unusual for the residential mortgage desk. Files get bounced.

This isn’t ideology. It’s underwriting economics. Big banks haven’t decided multiplex is a bad asset class — they’ve decided it doesn’t fit their machine.

Why credit unions are leaning in

Vancity’s CEO Wellington Holbrook framed the program around purpose: “We’re proving that with purpose-driven innovation, banking can help people.” That’s the public message. The deeper logic is structural.

Credit unions in BC have three advantages writing multiplex:

- Local underwriting. The credit officer reviewing a Kitsilano four-plex file actually knows Kitsilano. They can size land value, rental comps, and contractor quality without flying in an appraiser from Toronto.

- Member-driven mandate. Credit unions exist to lend to their members. A homeowner adding three rental units on their existing lot is the textbook profile.

- Asset class stickiness. Once a lender has 50 completed multiplex projects on its book, it has data on draw schedules, completion timelines, lease-up risk, and post-construction take-out. The next 50 projects are easier and better-priced. Banks that haven’t built that book are years behind.

Vancity’s Multiplex Construction Mortgage program — launched Fall 2025, expanded April 2026 — is the most visible example. Up to 80% loan-to-cost, 18 months interest-only during construction, flexible amortizations for co-owners, and rental offset to help qualify. Those terms are competitive with anything CMHC-insured for a deal of this size, without the MLI Select energy and affordability scoring overhead.

Prospera, Coast Capital, G&F Financial, and several BC community credit unions are running similar plays. The category is no longer one-lender-deep.

The Toronto data and what it tells us

The data point worth holding in your head: in Toronto, 3–5 unit small-plex builds have surpassed 100+ unit project starts for the first time on record. That’s a structural inversion of how the market has been built for 30 years.

The drivers are the same in Vancouver:

- High-rise pre-sale absorption has cratered

- Condo investor demand has weakened with higher rates and the federal foreign-buyer ban

- Multiplex doesn’t need a pre-sale market — it can be owner-occupied or built-to-rent

- Multiplex deals close in 12–18 months from financing to occupancy vs. 5–7 years for a high-rise

Lenders follow where deals close. Right now, that’s missing middle.

Practical implications if you own a Vancouver R1-1 lot

Three takeaways:

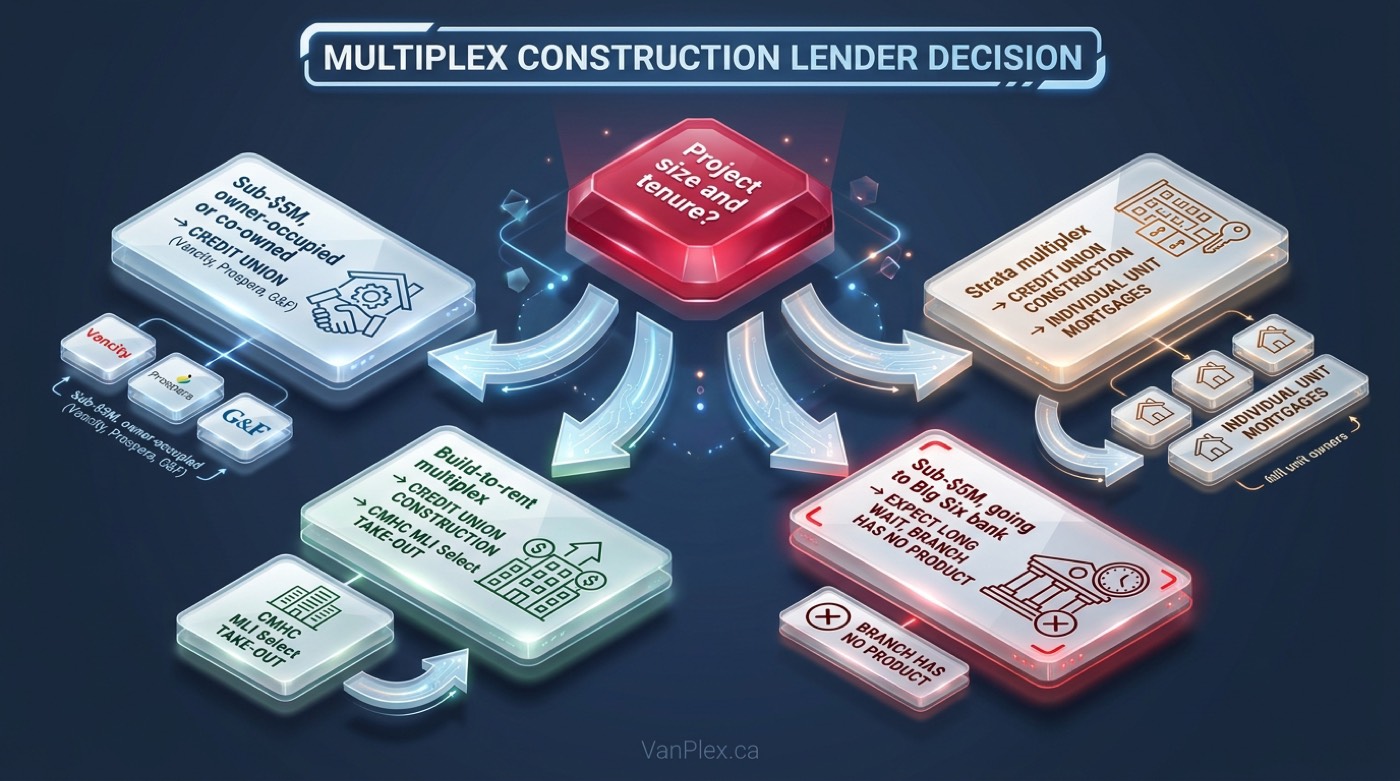

Start with credit unions, not banks

If you walk into a Big Six branch and ask for a multiplex construction loan on a $4M project, expect a long pause. The branch lender doesn’t have a product for you, and the construction lending desk that does is busy with $40M deals. Save yourself the cycle. Talk to Vancity, Prospera, or your local BC credit union first.

Understand what 80% LTC actually means

Vancity’s 80% loan-to-cost is the headline. The arithmetic: on a $4M project, you bring $800K in equity (often the lot, debt-free), the credit union finances $3.2M of construction. Interest-only during build. Then you take out the construction loan with either CMHC-insured term debt (if it’s purpose-built rental) or conventional residential mortgages on each strata unit (if it’s strata). The 80% LTC is real money — most BC homeowners with a paid-off lot and a multiplex plan can hit that threshold without a cash co-investor.

CMHC MLI Select still wins for build-to-rent — but credit unions get you there

The deepest discount on multi-unit financing is still CMHC MLI Select for build-to-rent — premium discount, 50-year amortization, the works. (See our CMHC MLI Select September 30, 2026 Energy Deadline post.) But MLI Select is the take-out on a stabilized rental project. The construction-phase financing — the loan you need to pour the foundation — typically comes from a credit union first, then refinances into the MLI Select-insured term loan after lease-up. Credit unions and CMHC aren’t competing. They’re sequenced.

For strata multiplex (sell each unit), credit unions handle construction; conventional residential mortgages on the buyers handle take-out. CMHC isn’t really in the picture.

What this means for the next 12 months

The shift toward credit unions writing multiplex isn’t a phase. It’s the shape of the market. As condo high-rise stays stuck, the supply pipeline that does move will be missing middle. The lenders that have built underwriting capability for that asset class will own the relationship with BC’s next 5,000 homeowner-developers.

For Vancouver and Burnaby owners considering a four-plex, six-plex, or laneway-and-suite combination, the practical next step is short: get a 30-minute call with a credit union construction lending specialist. Bring the lot address, a sketch of what you’re building, and an honest number on rental potential. They’ll tell you in that call whether the deal is bankable.

For a quick check on whether your specific Vancouver or Burnaby lot makes sense for a multiplex project — and what the financing stack realistically looks like — drop the address into the VanPlex proforma. It models construction-loan economics alongside take-out CMHC scenarios, so you can see both sides of the financing story.

Author: David Babakaiff, Co-Founder of VanPlex PlexRank™ | Profit with Multiplex

Sources:

- Canadian Mortgage Trends — As condo projects stall, multiplexes emerge as Toronto’s next supply engine

- Vancity — Multiplex home financing expansion announcement, April 8, 2026

- Western Investor — Why aren’t there more multiplexes under development in B.C.?

- Business in Vancouver — Vancouver’s multiplex market matures