Underwriting | CMHC MLI Select

CMHC MLI Select: What It Actually Does for Your Multiplex

MLI Select is not a grant. Not a subsidy. Not free money. It is mortgage loan insurance that rewards rental projects meeting social-good criteria with longer amortization, higher leverage, and lower premiums. You pay for it. The question is whether the math justifies the cost.

The Numbers That Matter

- ✓5-unit minimum. Fewer than 5 units and MLI Select does not exist for you.

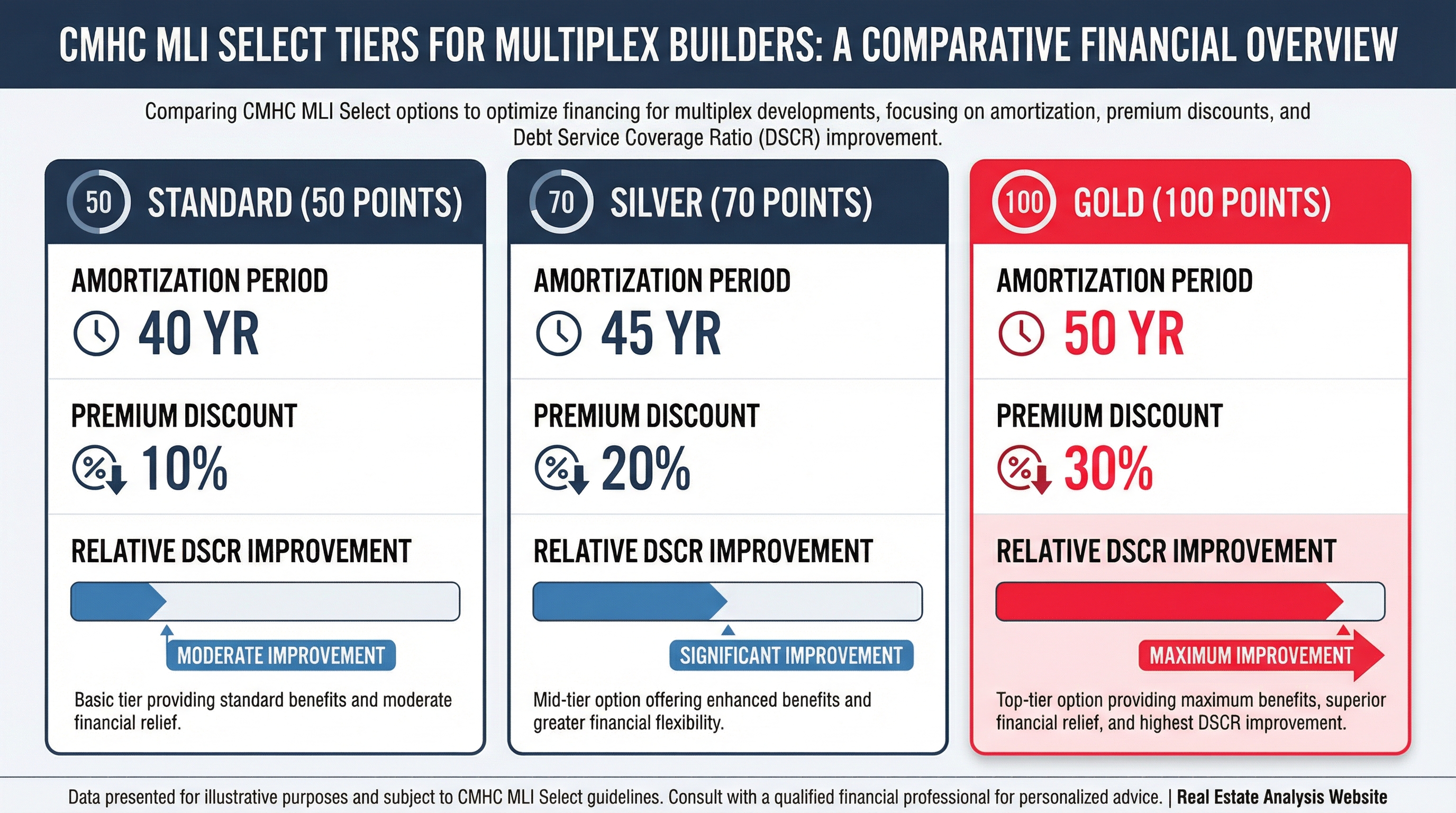

- ✓Three tiers: 50 points gets 40-year amortization. 70 points gets 45 years. 100 points gets 50 years.

- ✓Premium discounts: 10% off at 50 points, 20% at 70, 30% at 100. Applied after amortization surcharges.

- ✓Amortization surcharge: 0.25% added per 5-year increment above 25 years. A 50-year amort adds 1.25% to the premium.

What MLI Select Actually Is

CMHC insures your lender's loan. That insurance means the lender faces less risk, so they give you better terms: higher loan-to-value, longer amortization, lower interest rates. That is the entire mechanism.

You pay for this insurance through a premium calculated as a percentage of the insured loan amount. On a $1.2M loan, a 5% premium is $60,000. CMHC capitalizes the premium into the mortgage — you do not write a cheque — but the debt is real and the interest on it compounds over the full amortization period.

MLI Select replaced the older MLI Flex program on March 7, 2022. It added a points-based scoring system that rewards projects for affordability commitments, energy efficiency, and accessibility. Score higher, get better terms. The trade-off is that those commitments are binding for 10 to 20 years.

For a Vancouver 8-unit multiplex, MLI Select is often the difference between a deal that clears the 1.1x debt coverage ratio and one that does not. Conventional 25-year amortization produces monthly payments that most small rental buildings cannot support. Stretching to 40 or 50 years changes the monthly math enough to make the numbers work.

The Three Tiers

Every MLI Select project scores points across three categories. Hit a threshold, unlock the corresponding tier. The tiers are cumulative — 100 points includes everything 50 and 70 unlock, plus additional benefits.

50 Points — Entry Tier

2/540-year amortization. 10% premium discount. Minimum threshold to access MLI Select benefits. Most achievable for small multiplex builders.

70 Points — Enhanced Tier

3/545-year amortization. 20% premium discount. Requires meaningful commitments across affordability and energy efficiency. The sweet spot for most Vancouver 8-unit projects.

100 Points — Maximum Tier

5/550-year amortization. 30% premium discount. Limited-recourse option available. Requires deep affordability, near-net-zero energy, and accessibility commitments. Hard to hit without purpose-built social housing intent.

| Tier | Max Amort | Max LTV | Premium Discount | Min DCR | Recourse | Difficulty |

|---|---|---|---|---|---|---|

| 50 pts | 40 years | Up to 95% | 10% | 1.10x | Standard | Achievable |

| 70 pts | 45 years | Up to 95% | 20% | 1.10x | Standard | Moderate |

| 100 pts | 50 years | Up to 95% | 30% | 1.10x | Limited available | Demanding |

LTV applies to new construction and refinance scenarios. Existing property purchases may have lower LTV caps depending on property type. All tiers require a minimum 1.10x DCR. Premium discounts apply after amortization surcharges are added.

What Gets You Points

Three scoring categories. You can lean heavily on one or spread across all three. The mix-and-match flexibility is the most useful part of the system.

Affordability — Up to 100 Points

The highest-value category. Commit a percentage of units to rents at or below 30% of median renter household income for your area. The commitment must last a minimum of 10 years. Extend to 20 years and CMHC adds a 30-point bonus.

New Construction

- ▸ 50 pts: 10% of units at affordable rents

- ▸ 70 pts: 15% of units

- ▸ 100 pts: 25% of units

Existing Properties

- ▸ 50 pts: 40% of units at affordable rents

- ▸ 70 pts: 60% of units

- ▸ 100 pts: 80% of units

For an 8-unit new construction project, 50 points requires 1 affordable unit. 100 points requires 2 units. On existing properties, the bar is much higher. Rent increases during the commitment period are capped at the lower of provincial CPI or local legislation. Starting 2027, CMHC will require the lowest provincial CPI rate.

Energy Efficiency — Up to 50 Points

Points based on performance above the National Energy Code for Buildings (NECB) baseline. For new construction, the benchmark is NECB/NBC Tier 1. For existing buildings, it is your current energy performance.

New Construction

- ▸ 20 pts: 25% better than NECB Tier 1

- ▸ 35 pts: 50% better than Tier 1

- ▸ 50 pts: 60-70% better than Tier 1

Existing Properties

- ▸ 20 pts: 15% reduction from current

- ▸ 35 pts: 25% reduction

- ▸ 50 pts: 40% reduction

BC Energy Step Code alignment: Step Code 3 for Part 9 buildings (under 4 storeys) roughly maps to the 20-point threshold. Step Code 4 approaches the 35-point range. Net-zero-ready or Passive House certification typically exceeds the 50-point threshold. Most Vancouver multiplex projects already build to Step Code 3 minimum due to municipal requirements, so 20 energy points are often a baseline, not a stretch.

Accessibility — Up to 30 Points

The smallest category by point value, but often the easiest to achieve in a new build. CMHC requires 100% of units to be visitable as a baseline. Points come from going further.

- ▸ 20 pts: 15% of units fully accessible per CSA B651:23 standards, OR Rick Hansen Foundation score of 60-79%

- ▸ 30 pts: 15% accessible units + 85% universal design features, OR Rick Hansen Foundation Gold certification (80%+)

For an 8-unit building, 15% means 2 accessible units (rounded up). Universal design features include wider doorways (36"), lever handles, roll-in showers, and lowered countertops. In a new build, designing these features into the ground-floor units adds minimal cost — roughly $3,000-5,000 per unit — and scores 20-30 points.

Scoring a Vancouver 8-Unit: A Realistic Path to 70 Points

An 8-unit secured rental multiplex in Vancouver. The builder wants 70 points to access 45-year amortization and a 20% premium discount. Here is one realistic path:

Energy

20 pts

BC Step Code 3+ (already required by Vancouver for new multi-unit). Achieves 25%+ above NECB Tier 1.

Accessibility

20 pts

2 ground-floor units built to CSA B651 barrier-free. 100% visitable (required baseline). Cost: ~$8,000 total.

Affordability

30 pts

No affordability rent caps taken. Instead, extend the 10-year minimum commitment to 20 years for the +30 bonus points.

Total: 70 points. No unit-level rent caps. The only binding commitment is the 20-year affordability window, which in this path means maintaining the building as rental for 20 years — a timeline most BTR builders already plan for. Energy and accessibility requirements are met through standard construction practices and two barrier-free units.

The 5-Unit Minimum

The Hard Line

MLI Select requires a minimum of 5 self-contained residential units. Not beds. Not rooms. Self-contained units with their own kitchen, bathroom, and entrance.

A 4-unit building cannot use MLI Select. A 4-unit building with a secondary suite that does not meet CMHC's definition of self-contained does not count as 5.

This single rule is why unit count is the first thing to check on any BTR feasibility analysis. If the lot cannot support 5+ units under the applicable zoning, the CMHC financing advantage does not exist.

Why Vancouver's 8-Unit Path Matters

Vancouver's R1-1 secured rental policy allows up to 8 units on standard 33-foot lots and more on wider lots. That is 3 units above the MLI Select minimum.

The margin matters. At 5 units, you barely qualify and one unit reclassification during CMHC review could disqualify the project. At 8 units, you have buffer.

Other BC municipalities that allow 6+ unit multiplex under Bill 44 also clear the threshold. But check the specific zoning — Bill 44 mandates municipalities allow small-scale multi-unit housing, it does not guarantee 5+ units on every lot.

What MLI Select Does NOT Fix

MLI Select is a financing tool. It optimizes the debt structure. It does not change the fundamental economics of the project.

Overpaid land

MLI Select does not fix overpaid land. If you bought the lot at strata pricing, longer amortization lowers your monthly payment but does not change the fact that the yield on cost is inadequate. A 50-year amortization on a $2.5M lot that needed to be $1.7M still produces a sub-economic return.

A rent roll that cannot service the debt

If stabilized rents cannot cover operating expenses plus debt service at a 1.1x DCR, no amortization extension changes that outcome. It moves the line, but it does not create income that is not there.

Fewer than 5 units

There is no waiver, no exception, no workaround. Four units means conventional financing: 25-year amortization, lower LTV, higher rates, personal guarantee. The economics are fundamentally different.

The total interest cost of longer amortization

A 50-year amortization at 3.5% on a $1.2M mortgage means you pay $1.34M in total interest over the life of the loan. A 25-year amortization on the same loan costs $585K in total interest. The difference is $755K. Longer amortization improves monthly cash flow. It does not reduce your cost of capital — it increases it substantially.

How Tier Choice Changes the Math

Same 8-unit building. Same $1.1M insured mortgage. Same 3.5% rate. Same $65,000 NOI. The only variable is amortization, driven by which MLI Select tier you qualify for.

| Scenario | Amort | Monthly Pmt | Annual DS | DCR | Result |

|---|---|---|---|---|---|

| No MLI Select (Conventional) | 25 yrs | $5,830 | $69,960 | 0.93x | Fails |

| 50 pts — 40-Year Amort | 40 yrs | $4,270 | $51,240 | 1.27x | Passes |

| 70 pts — 45-Year Amort | 45 yrs | $4,060 | $48,720 | 1.33x | Passes |

| 100 pts — 50-Year Amort | 50 yrs | $3,890 | $46,680 | 1.39x | Comfortable |

Based on $1.1M insured mortgage, 3.5% interest rate, $65,000 annual NOI. Your actual numbers will vary based on construction cost, rent levels, and operating expenses. Use VanPlex's BTR calculator to model your specific property.

The takeaway: Without MLI Select, this building fails the DCR test at 0.93x. At 50 points (40-year amort), it passes at 1.27x. The jump from conventional to MLI Select entry tier is the most significant threshold. Moving from 50 to 100 points adds comfort margin but the binary pass/fail decision happens at the first tier.

Premium Cost: The Real Numbers

CMHC updated MLI Select premiums effective July 14, 2025. The structure is: base LTV premium + amortization surcharge - tier discount = your premium.

Base Premium

At 85% LTV for a stabilized purchase. Construction loans start around 6-7%. Higher LTV means higher base premium. At 95% LTV, base is approximately 6.15%.

Amort Surcharge

30 years: +0.25%. 40 years: +0.75%. 45 years: +1.00%. 50 years: +1.25%. An additional +0.25% EGI surcharge applies if your building has not reached projected income at first advance.

Tier Discount

Applied after surcharges. 50 pts: 10% off. 70 pts: 20% off. 100 pts: 30% off. The discount partially offsets the amortization surcharge but does not eliminate it.

Worked Example: $1.2M Loan, 85% LTV, 40-Year Amort, 70 Points

Base premium (85% LTV, stabilized): 5.35%

Amortization surcharge (40 yrs = +3 increments): +0.75%

Subtotal: 6.10%

70-point discount (20% off 6.10%): -1.22%

Final effective premium: 4.88%

Dollar amount on $1.2M: approximately $58,560, capitalized into the mortgage.

Best For

- ✓ Rental multiplex projects with 5 or more self-contained units that can realistically score 50+ points through energy efficiency, accessibility, or affordability commitments.

- ✓ Vancouver 8-unit secured rental builds where the 40-50 year amortization is the difference between passing and failing the 1.1x DCR test.

- ✓ Builders already meeting BC Energy Step Code 3+ and willing to incorporate 2 barrier-free ground-floor units — a low-cost path to 40-50 points.

Usually Fails When

- ✕ The project has fewer than 5 units. No workaround exists.

- ✕ The land basis is too high for rental economics regardless of amortization length.

- ✕ The builder cannot meet even the minimum energy or accessibility thresholds and is unwilling to commit to affordability rent caps.

- ✕ The pro forma only works at 100 points but the project realistically scores 50. Do not underwrite financing terms you cannot achieve.

What To Verify Before Spending Money

- → Confirm unit count is 5 or more self-contained units per CMHC definition before any other analysis.

- → Score your project across all three categories. Be honest about what you can achieve, not what you hope to achieve.

- → Model the deal at the tier you can realistically hit, not the tier you want. Use VanPlex's BTR calculator to see the DCR impact.

- → Budget for the insurance premium as a real cost. It gets capitalized into the mortgage but it increases total debt and total interest paid over the amortization period.

Frequently Asked Questions

Can a 4-unit multiplex qualify for MLI Select?

How much does the CMHC insurance premium actually cost?

What is the easiest way to reach 50 points?

Does MLI Select work for a building I already own?

What happens if I commit to affordability rents and the market drops below those rents?

How does VanPlex model MLI Select in its BTR calculator?

Related Reading

CMHC MLI Select for Small Builders: The 2026 Guide

The complete guide to MLI Select tiers, premium discounts, and how small multiplex projects qualify.

The 5-Unit Threshold: Why It Changes Everything for Multiplex Financing

How crossing from 4 to 5 units unlocks CMHC commercial insurance, longer amortization, and lower rates.

Official Sources Referenced

Screen Your Lot for Build-to-Rent

Enter any BC address to compare rental hold potential, unit count, and the for-sale alternative before you spend money on drawings.