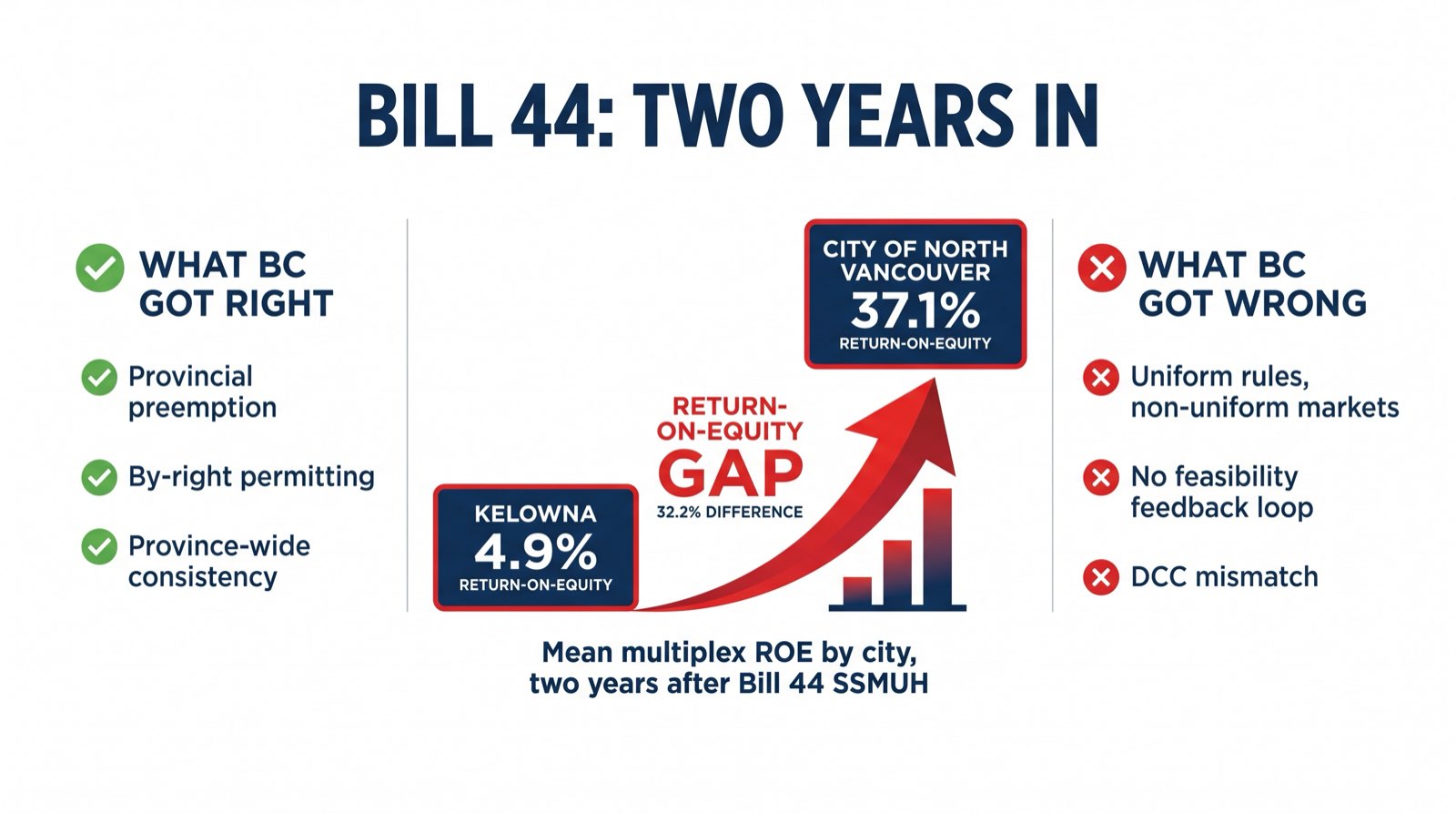

Same province. Same Bill 44 floor. Different math.

Kelowna and Vancouver both sit under BC’s Small-Scale Multi-Unit Housing framework. Both hit the compliance deadline. Both pre-zoned their residential maps for 4- to 6-unit as-of-right density on eligible lots. If you stop the analysis there, you’d expect proformas to rhyme. They don’t.

The land basis is different. The rents are different. The vacancy is different. The exit liquidity is different. The climate and wildfire overlay is different. This post walks through what’s actually the same, what’s actually different, and which owner profile should play in which city.

The baseline: what Bill 44 gave both cities

The Housing Statutes (Residential Development) Amendment Act set identical minimum unit-count floors across BC:

- 3 units on lots ≤ 280 m²

- 4 units on lots > 280 m²

- 6 units on lots > 280 m² near qualifying frequent transit

Both cities are compliant. Kelowna hit the floor on March 18, 2024, ahead of the June 30, 2024 deadline. Vancouver did the same through its R1-1 zone.

That’s where the match ends.

The comparison table

| Dimension | Kelowna | Vancouver |

|---|---|---|

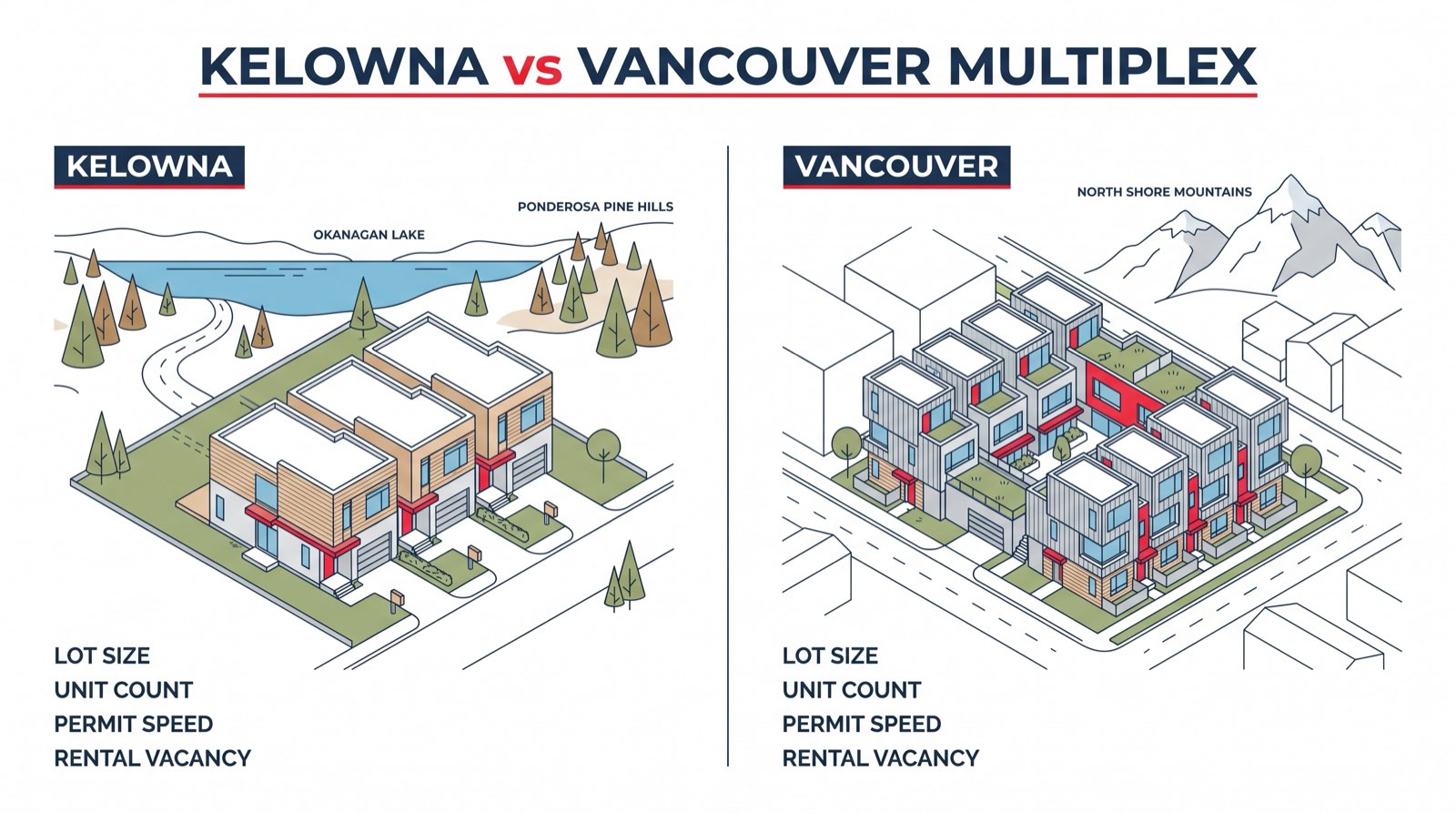

| Typical lot size | 550-700 m² | 370-460 m² |

| SSMUH unit count (Bill 44 floor) | Up to 6 | Up to 6 |

| Max unit count with secured rental | 6 (SSMUH) | Up to 8 (R1-1 secured-rental) |

| Permit approval speed | Fast-Track + no public hearing for SSMUH | Longer review cycles, staff capacity constrained |

| Avg 2-bed market rent (2025) | $2,118 | Materially higher |

| CMA vacancy (2025) | 6.4% | ~1.2% |

| Exit market depth | Thinner | Deeper |

| Wildfire/climate overlay | Material (FireSmart, overheating) | Minor |

| Land basis per buildable unit | Lower | Higher |

Sources: CMHC 2025 Kelowna Rental Market data, Province of BC housing data release, Kelowna FireSmart program, Kelowna Step Code / HDD data.

Where the math diverges

Land basis

Kelowna’s typical residential lot is 30-50% larger than Vancouver’s Westside or East Van standard parcel. That bigger footprint matters in two directions:

- More buildable area per dollar of land

- More expensive total dirt per acquisition, even at lower per-m² pricing

A 650 m² Kelowna South lot and a 400 m² Vancouver Westside lot both deliver a 6-unit SSMUH build under Bill 44. The Kelowna build has materially more floor area to distribute across those units. That reshapes unit mix, rent ceiling, and construction cost per door.

Rent

CMHC’s 2025 numbers for Kelowna CMA:

| Unit type | Kelowna 2025 avg |

|---|---|

| Studio | $1,395 |

| 1-bed | $1,596 |

| 2-bed | $2,118 |

| 3-bed | $2,895 |

Vancouver’s 2025 rents run materially higher across every unit type. The gap is widest on 1-bed and 2-bed, narrower on 3-bed where Kelowna’s larger unit footprints earn closer rent parity.

The rent gap is what funds Vancouver’s higher land basis. It’s also what makes Kelowna proformas more sensitive to vacancy than to rent growth assumptions.

Vacancy

This is the biggest single difference in the 2025 underwriting environment.

- Kelowna CMA: 6.4%, City of Kelowna 6.9%, Rutland 7.5%, West Kelowna 5.3%

- Vancouver: roughly 1.2%

A 5-point vacancy gap isn’t a rounding error. It’s the difference between aggressive lender underwriting and conservative lender underwriting. It’s the difference between 3-month lease-up and 9-month lease-up. It’s the difference between a 4-plex that stabilizes in its first calendar year and one that doesn’t.

Kelowna is a looser market. That loosens exit assumptions and tightens debt service coverage math in ways a builder has to underwrite honestly.

Permit speed

Kelowna runs an Infill Fast-Track program for SSMUH-conforming applications. No public hearing, Planning staff review, envelope-based compliance. Timelines from complete application to building permit are routinely weeks rather than months for clean projects.

Vancouver’s permitting queue is thicker. Even for Bill 44-conforming R1-1 projects, staff capacity and review cycles run longer. The time-cost of capital on a 12-month extra hold is real.

Exit liquidity

Vancouver has a deeper multi-unit buyer pool. Family offices, REITs, immigrant-capital buyers, and small-scale syndicates compete for stabilized small-building product. Cap rates reflect that depth.

Kelowna’s buyer pool for stabilized 4-8 unit product is thinner. It’s real — CMHC MLI Select takeouts pull in out-of-province and institutional buyers — but it’s shallower than Lower Mainland depth. Builders planning exits at stabilization should stress-test cap rate widening. The right frame isn’t “can I exit?” — it’s “what’s the cap rate discount I have to price in?”

The depth differential also shapes financing. Vancouver construction lenders price Lower Mainland risk aggressively because they can refinance or sell participations if needed. Kelowna lenders on the same deal quote wider spreads or tighter loan-to-cost ratios because the liquidity backstop is thinner. That delta shows up in the equity requirement, not just the exit number.

Climate and wildfire overlay

Kelowna’s climate overlay is the single biggest underwriting input Vancouver operators underestimate:

- HDD of 3,715, higher than Vancouver’s heating load

- 26°C overheating rule for one living space per unit, which forces mechanical cooling on most new builds

- FireSmart Priority Zone 1 requirements within 10 m of any structure

- Post-McDougall Creek wildfire (August 2023) insurance conditionality

A Vancouver builder flying into Kelowna and speccing cedar lap siding, wood-shake roofing, and a passive-cooling envelope without active mechanical will fail envelope review on FireSmart, Step Code, or both. The climate delta is a line item.

Three owner profiles

Profile 1: “Go Kelowna”

You should lean Kelowna if:

- Your capital is patient (3-5 year hold, not flip)

- You want larger units and family-household rental exposure

- You can operate a wildfire-interface envelope correctly

- You have a CMHC MLI Select takeout plan to absorb lease-up

- Your equity-return math survives a 6-9 month stabilization

Best Kelowna targets: Core Area lots in Pandosy and Kelowna South, Rutland transit-corridor lots, North Glenmore UBCO-driver parcels.

Profile 2: “Stay Vancouver”

You should lean Vancouver if:

- Your capital wants the shortest stabilization runway available

- You want rent ceilings above Kelowna’s CMHC averages

- You can underwrite the longer permit cycle

- You want access to the deepest exit buyer pool

- You’re comfortable at sub-2% vacancy working against you on tenant-sourcing and CCAP-style friction

Best Vancouver targets: Broadway-adjacent R1-1 lots, East Van corridor lots, Westside 8-unit secured-rental plays.

Profile 3: “Operate in both”

The 3-5 build/year operator who can run parallel teams — one Lower Mainland, one Okanagan — captures advantages from both markets:

- Vancouver for velocity and exit depth

- Kelowna for larger unit product and land basis per door

- Diversified weather/climate exposure (Vancouver crews can’t work Okanagan envelopes cold)

- Staggered cash-flow cycles across two submarkets

This profile needs enough volume to justify the ops overhead. Typically 6+ builds per year combined.

The housing-target backdrop

BC assigned Kelowna a housing target of 8,774 new homes for 2024-2029. Vancouver carries a much larger target, matched to its much larger population base. But the per-capita pressure is in the same order of magnitude, and both municipalities face Provincial performance review if they miss.

That matters to a multiplex builder for one reason: Planning staff in both cities are under direct political pressure to approve SSMUH-conforming applications quickly. That’s a tailwind in both markets. It’s a bigger tailwind in Kelowna because the underlying Planning queue was thinner to start with, but it’s real in both cities.

The 2021 Census put Kelowna CMA at 222,162 residents. That’s a fraction of Metro Vancouver’s population, but Kelowna has been among the fastest-growing CMAs in the country. Demand is compounding; what Bill 44 did was ensure the zoning frame could absorb that demand without bespoke rezoning on every lot.

What the comparison doesn’t capture

Two things this post deliberately skips.

The Infill Fast-Track program deserves its own treatment — it’s the operational reason Kelowna timelines beat Vancouver timelines on SSMUH-conforming builds, and the details of what qualifies matter.

Kelowna DCCs under Bylaw 12420 run on four residential brackets (Res 1-4 by units per hectare). That schedule doesn’t map cleanly to Vancouver’s CAC / DCL regime, and the comparison needs more than a single paragraph.

The position

Vancouver is a rent-growth and exit-liquidity market. Kelowna is a land-basis and patient-capital market. Same Bill 44 floor, different capital stacks, different timelines, different operator profiles.

The mistake is importing one city’s playbook wholesale into the other. A Vancouver 6-plex operator who locks Kelowna land at Vancouver debt service assumptions will stall. A Kelowna builder chasing Vancouver’s rent ceiling will build unit mixes that mis-price against local demand.

Key takeaway: The zoning is the same in both cities. Everything downstream of zoning is not.

Related reading

- Kelowna vs Vancouver multiplex comparison

- Kelowna Infill Fast-Track explained

- Kelowna rental market data

- Build-to-rent multiplex strategy

What’s next for your Kelowna lot

The Kelowna Multiplex hub walks through zoning, neighbourhoods, rent comps, and proforma math specific to the Okanagan. If you’re operating in both markets or evaluating the jump from Vancouver, run a lot through the analyzer to see the math on your specific parcel.