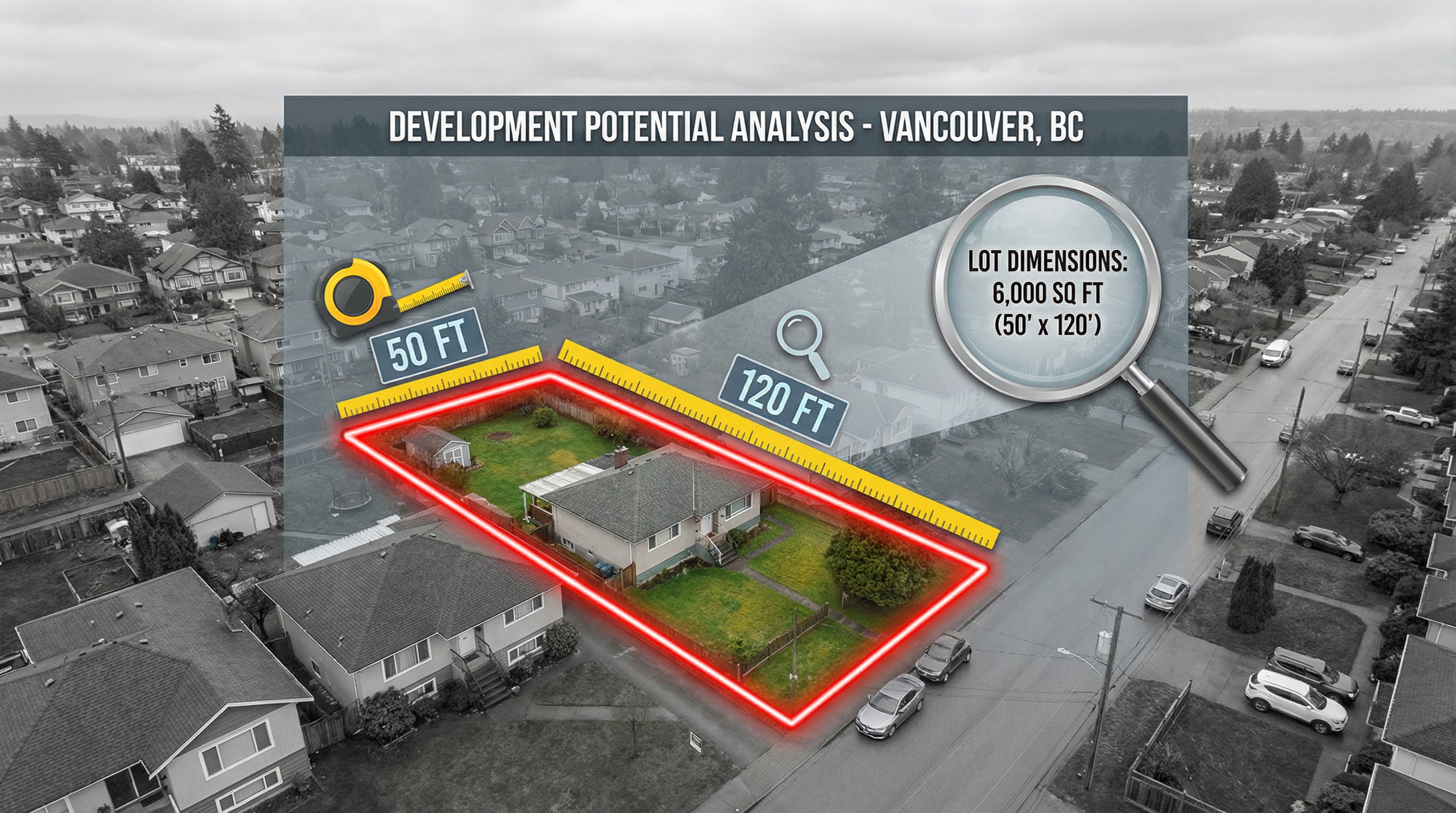

Same lot. Same neighbourhood. Two completely different businesses. Here’s what both proformas look like on a real Vancouver property — a 6,200 sq ft R1-1 lot on the East Side, purchased for $1.85M.

TL;DR (Key Takeaways)

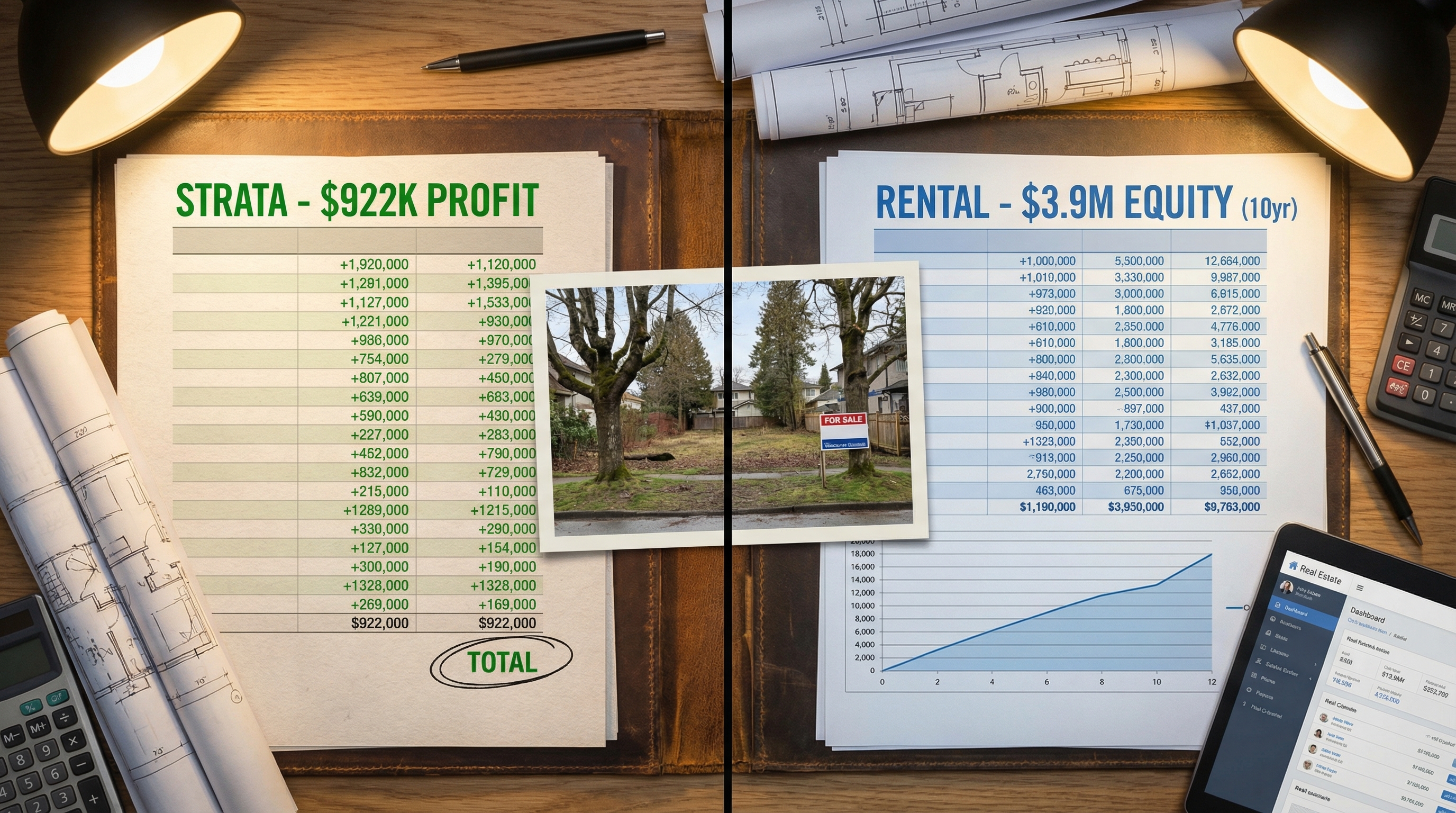

- Strata (build-to-sell): 6 units, conventional financing, $4.89M total cost, $5.88M in sales, ~$990K profit in 18-20 months

- Rental (build-to-rent): 8 units at 1.00 FSR, CMHC MLI Select, $4.12M total cost, 5.2% stabilized cap rate, ~$125K equity in

- Strata gives you cash now: ~20% return on cost, taxable as income or capital gains

- BTR gives you a compounding asset: Year 1 cash flow is thin, but by year 10 you own $6M+ in real estate with $3M+ in equity

- The break-even point where BTR’s accumulated wealth surpasses strata profit is approximately year 7-8

The Lot

6,200 sq ft (576 m2) in the Renfrew-Collingwood area of East Vancouver. R1-1 zoning. 50.2 ft frontage (15.3m). Current assessment: $1.85M. Existing 1960s bungalow. Transit score: high — 2 blocks from a frequent bus route, qualifying for 6-unit base density.

Under R1-1, this lot supports:

- Market strata: Up to 6 units at 0.70 FSR = 4,340 sq ft buildable

- Secured rental: Up to 8 units at 1.00 FSR = 6,200 sq ft buildable

Both options are by-right under current zoning. No rezoning required. No public hearing.

Proforma A: Build-to-Sell (Strata)

Development Costs

| Line Item | Amount |

|---|---|

| Land acquisition | $1,850,000 |

| Hard costs (4,340 sf x $425/sf) | $1,844,500 |

| Soft costs (design, engineering, permits) | $285,000 |

| Density bonus contribution ($82,000 x 6 units) | $492,000 |

| Construction financing (12 months at 7.5%) | $138,400 |

| Marketing and sales commissions (3.5%) | $205,800 |

| Contingency (5% of hard costs) | $92,225 |

| Total project cost | $4,907,925 |

Revenue

Six strata units. Based on Q1 2026 comparable sales for new-build multiplex strata in East Vancouver:

| Unit Type | Count | Size (sf) | Price/Unit | Revenue |

|---|---|---|---|---|

| 2-bed + den (ground) | 2 | 850 | $1,050,000 | $2,100,000 |

| 2-bed (upper) | 2 | 720 | $975,000 | $1,950,000 |

| 1-bed (upper) | 2 | 580 | $890,000 | $1,780,000 |

| Total gross revenue | $5,830,000 |

Returns

| Metric | Value |

|---|---|

| Gross revenue | $5,830,000 |

| Total cost | $4,907,925 |

| Pre-tax profit | $922,075 |

| Return on cost | 18.8% |

| Equity invested (20% of costs excl. land) | ~$610,000 |

| Return on equity | ~151% |

| Timeline | 18-20 months |

That $922,075 is taxable. If structured as a development corporation, the combined federal-provincial corporate rate in BC is approximately 27%. After-tax profit: approximately $673,000. If taxed personally as business income, you’re looking at marginal rates of 49-53% on the top portion in BC.

The strata model is a construction business. You buy materials, add labour, sell a finished product for more than it cost. The profit is real, it’s immediate, and it’s taxed like income.

Risk Factors

Strata sales depend on buyer demand at closing. If the market softens between your purchase and completion — as it has in 2025-2026 for condos — you’re holding finished inventory with carrying costs. Presale requirements from lenders may slow your timeline. The density bonus contribution of $492,000 is a hard cost that doesn’t exist in the rental path.

Proforma B: Build-to-Rent (Secured Rental, CMHC MLI Select)

Development Costs

| Line Item | Amount |

|---|---|

| Land acquisition | $1,850,000 |

| Hard costs (6,200 sf x $425/sf) | $2,635,000 |

| Soft costs (design, engineering, permits, energy modelling) | $310,000 |

| Density bonus contribution | $0 (exempt for secured rental) |

| Construction financing (14 months at 7.5%) | $230,500 |

| CMHC insurance premium (5.72% of mortgage) | $131,100 |

| Contingency (5% of hard costs) | $131,750 |

| Total project cost | $5,288,350 |

Wait — the rental project costs more? Yes. You’re building 1,860 sq ft more (6,200 vs 4,340). More units, more plumbing, more kitchens. But you also eliminate the $492,000 density bonus contribution, which partially offsets the additional construction cost.

Financing (CMHC MLI Select — 70 points)

| Parameter | Value |

|---|---|

| CMHC appraised value / cost basis | $5,288,350 |

| LTV | 95% |

| Mortgage amount | $5,023,933 |

| Amortization | 45 years |

| Interest rate | 4.25% (5-year fixed) |

| Monthly payment | $21,750 |

| Annual debt service | $261,000 |

| Equity required | $264,417 |

Your equity in is $264,417. The CMHC-insured mortgage covers the rest. Compare to the strata model’s $610,000 equity requirement.

Operating Income (Stabilized — Year 1)

| Line Item | Monthly | Annual |

|---|---|---|

| 3 x 2-bed units @ $2,800 | $8,400 | $100,800 |

| 3 x 1-bed units @ $2,350 | $7,050 | $84,600 |

| 1 x studio @ $1,950 | $1,950 | $23,400 |

| 1 x affordable unit (30% median income) | $1,400 | $16,800 |

| Gross rental income | $18,800 | $225,600 |

| Vacancy (4%) | ($9,024) | |

| Property management (8%) | ($18,048) | |

| Property tax | ($14,200) | |

| Insurance | ($8,500) | |

| Maintenance reserve (5%) | ($11,280) | |

| Net Operating Income | $164,548 |

CMHC Qualification Check

| Test | Requirement | Actual | Result |

|---|---|---|---|

| DSCR | >= 1.10 | $164,548 / $261,000 = 0.63 | FAIL |

The DSCR fails at 95% LTV. This is the reality check that many BTR proformas skip. Let’s adjust.

Revised Financing — 85% LTV

| Parameter | Value |

|---|---|

| LTV | 85% |

| Mortgage amount | $4,495,098 |

| Annual debt service | $233,600 |

| Equity required | $793,253 |

| Test | Requirement | Actual | Result |

|---|---|---|---|

| DSCR | >= 1.10 | $164,548 / $233,600 = 0.70 | FAIL |

Still fails. The land cost at $1.85M is too high relative to rental income. Let’s see what LTV actually works.

What LTV Clears DSCR?

For a 1.10 DSCR, annual debt service must be below $149,589. Working backwards with 45-year amortization at 4.25%, that requires a mortgage of no more than approximately $3,452,000 — or 65% of total project cost.

Equity required at 65% LTV: $1,850,923.

That’s nearly the entire land cost in equity. At this point, BTR doesn’t pencil as a leveraged play — it becomes a cash-heavy hold strategy. This is the honest math.

When Does BTR Work on This Lot?

BTR works on this lot under specific conditions:

Scenario 1: You already own the land. If the $1.85M lot is already yours (inherited, or you’re redeveloping your own home), the equity requirement drops dramatically. Your “cost” is opportunity cost, not cash outlay. CMHC underwrites based on appraised value, and with land already owned, the LTV calculation changes.

Scenario 2: Land cost is lower. At $1.2M land cost, total project cost drops to $4.64M. A 95% LTV mortgage of $4.41M has annual debt service of $229,000. DSCR = $164,548 / $229,000 = 0.72. Still fails. The rent levels in Renfrew-Collingwood aren’t high enough for pure BTR on acquired land.

Scenario 3: Higher-rent neighbourhood. In Mount Pleasant or Grandview-Woodland, 2-bed rents hit $3,200-3,400 for new-build. Gross income on the same 8-unit mix climbs to $265,000+, pushing NOI to $195,000+. DSCR at 85% LTV: $195,000 / $233,600 = 0.83. Closer, but still tight.

The reality: pure BTR on acquired land in Vancouver works in a narrow band of lots where land cost is low relative to achievable rents and unit density is maximized. For most East Vancouver lots at current land prices, strata is the better financial outcome.

The 10-Year Comparison

Despite the DSCR challenge, let’s model the owner-occupied scenario — the homeowner who already lives on the lot and redevelops it. Land cost: $0 cash outlay (opportunity cost only). Total hard + soft + financing: $3,438,350.

At 95% LTV on $3,438,350: mortgage of $3,266,433. Annual debt service: $169,700. DSCR = $164,548 / $169,700 = 0.97. Still below 1.10, but with owner-occupied adjustments and CMHC’s flexibility on new construction, borderline projects can sometimes get approved with additional equity or rent upside demonstrated.

Assume the project proceeds at 85% LTV with $515,753 equity in:

Year 1-5: Thin cash flow. NOI rises 3% annually with rent growth. Mortgage stays fixed for the 5-year term. By year 5, NOI is $190,700.

Year 5-10: Refinance at then-current rates. Building value appreciates. By year 10, the building is worth approximately $6.5M (4% annual appreciation on $4.4M stabilized value). Mortgage balance has amortized to approximately $2.6M. Your equity position: $3.9M.

Strata comparison at year 10: You took your $673,000 after-tax profit, reinvested it. Even at 8% annual returns in the market, it’s worth approximately $1.45M.

BTR wins at year 10: $3.9M vs $1.45M.

But you needed a different entry point — existing land ownership, not $1.85M in acquisition cost.

The Decision Framework

| Factor | Strata (Sell) | BTR (Hold) |

|---|---|---|

| Cash required | ~$610K | ~$125K-$800K (varies by LTV) |

| Time to liquidity | 18-20 months | 10+ years |

| Ongoing effort | None after sale | Property management, tenants |

| Tax treatment | Income/capital gains | Rental income + depreciation |

| Upside exposure | Fixed at sale price | Appreciation + rent growth |

| Downside risk | Market softens pre-sale | Vacancy, rate resets, maintenance |

| Best for | Capital recyclers, active developers | Long-term holders, existing landowners |

There is no universally correct answer. The right choice depends on your land basis, your capital position, your tax situation, and your timeline.

If you acquired the land at market price and need a return within 2 years: sell.

If you own the land already and have a 10+ year horizon: hold.

If you’re somewhere in between: run both proformas with your actual numbers. (Use VanPlex’s BTR analyzer to model your lot)

David Babakaiff is the Co-Founder and CEO of VanPlex, a Vancouver-based company specializing in multiplex development and Missing Middle housing. VanPlex uses its AI-powered PlexRank system to identify and underwrite multiplex conversion opportunities under BC’s Bill 44 zoning reforms.

Run both proformas on your lot at VanPlex.ca.