You build an 8-unit multiplex under Vancouver’s R1-1 secured rental zoning. You hold it. You collect rent. The CMHC mortgage amortizes. Everything goes according to plan.

Then, 15 years in, you want to sell two units to fund your kid’s down payment. You can’t.

That’s the exit problem. And if you’re going into build-to-rent without understanding it fully, you’re making a permanent decision with incomplete information.

TL;DR (Key Takeaways)

- Secured rental tenure is permanent — you cannot stratify and sell units individually, ever

- Your building is valued by cap rate, not by what individual units would fetch on the open market

- A $158K NOI building at 4.75% cap rate = $3.33M — but those same 8 units sold individually as strata might total $5.2M+

- The gap between portfolio value and unit-by-unit value can exceed $1.5M on an 8-unit building

- The hold is still worth it in specific circumstances — but you need to go in with eyes open

What Secured Rental Tenure Actually Means

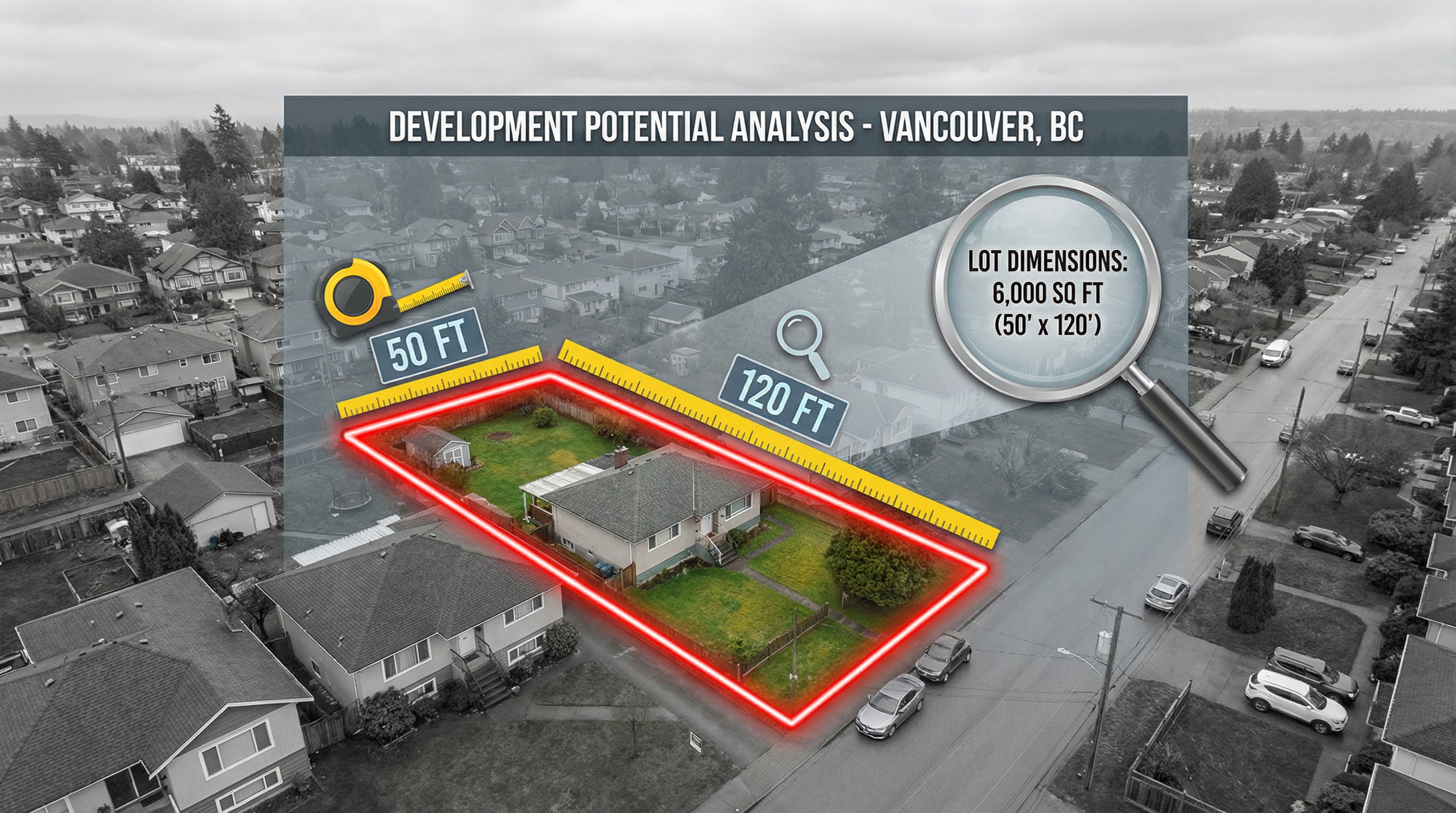

When you build under Vancouver’s secured rental density bonus (1.00 FSR instead of 0.70 FSR, 8 units instead of 6), the City registers a covenant on title. That covenant restricts the tenure of every unit to rental. Not for 10 years. Not for 20. Permanently.

BC enacted residential rental tenure zoning authority in July 2018. Municipalities can apply it to an area, a building, or individual units. Once applied, those units cannot be occupied by the owner and cannot be sold individually as strata.

You own the whole building. You can sell the whole building. You can refinance the whole building. You cannot carve it up.

This is not a technicality you can lawyer around later. It’s a permanent structural constraint on the asset.

Cap Rate Valuation vs Unit-by-Unit Sale

Here’s where the math gets uncomfortable.

An 8-unit secured rental building in East Vancouver. NOI of $158,000/year. At the prevailing cap rate for small rental buildings in non-premium Vancouver neighbourhoods — call it 4.75% — the building is worth $3.33M.

Now imagine those same 8 units as strata. New-build 2-bedroom condos in East Vancouver sell for $650,000-$750,000. One-bedrooms: $500,000-$580,000. A realistic unit mix of four 2-beds and four 1-beds, sold individually:

4 x $700,000 + 4 x $540,000 = $4.96M

The gap: $1.63M. That’s not a rounding error. It’s the permanent cost of the secured rental covenant.

A 14-unit building in Kitsilano recently traded at a 3.4% cap rate — but that’s Kitsilano, one of Vancouver’s most desirable rental markets with historically low vacancy. Your 6-8 unit building in Hastings-Sunrise or Renfrew-Collingwood isn’t getting 3.4%. It’s getting 4.5-5.0%, maybe higher if vacancy is elevated at time of sale.

The Wealth Accumulation Argument

So why would anyone accept this trade-off?

Because the hold model compounds. And over long enough horizons, the compounding wins — for specific situations.

Year 1 of an 8-unit BTR: you’re cash-flow neutral or slightly negative. Your DSCR is 1.10-1.15. After property management, maintenance reserves, and vacancy, there’s almost nothing left.

Year 10: the CMHC mortgage has amortized significantly. Rents have grown (even conservatively at 2.5%/year, your gross revenue is 28% higher). Your NOI is now $210,000+. Cash flow is positive. The building is worth more.

Year 25: the mortgage is paid off. You own a debt-free building generating $280,000+ in annual NOI (assuming modest rent growth and stable operations). The building, at a 4.5% cap rate, is worth $6.2M. You paid $4.9M total cost to build it.

The strata alternative: you sold 6 units (remember, no density bonus) for $3.8M total, netted $900K profit after costs, and invested that in something else. Over 25 years at 7% annual return, that $900K grew to $4.88M.

$6.2M debt-free building + $280K annual income vs $4.88M in a portfolio. The BTR wins — but only at the 25-year horizon. At 10 years, it’s close to a wash. At 7 years, strata wins.

When the Hold Is Not Worth It

BTR is wrong for you if:

You need liquidity within 10 years. The building’s cap rate valuation won’t exceed your total cost basis for roughly 8-12 years, depending on rent growth and cap rate compression. Selling before that means selling at or below cost.

Your estate plan requires divisible assets. You can’t leave Unit 3 to your daughter and Unit 7 to your son. You leave the whole building or you sell it. For families wanting to divide real estate among heirs, strata is more flexible.

The location doesn’t support rent growth. BTR’s compounding engine is rent growth. If your building is in a neighbourhood where rents stagnate — because of oversupply, demographic shifts, or transit changes — the 25-year math deteriorates badly. Vancouver’s 2025 vacancy spike to 3.7% (highest since 1988) is a warning signal, even if temporary.

You can’t tolerate operational burden. A rental building is an operating business. Property management costs 8-10% of gross revenue. Tenant turnover costs $2,000-$4,000 per unit per occurrence. The BC Residential Tenancy Act governs every interaction. This is not passive in any meaningful sense.

When the Hold Is Worth It

BTR makes financial sense when:

You already own the land. At zero land basis, the DSCR clears easily and cash flow is positive from year one. The gap between portfolio value and strata value still exists, but you’re not carrying $1.5M+ in land cost.

You have a 20+ year horizon. The compounding of mortgage paydown, rent growth, and asset appreciation needs two decades to fully express. The math is unambiguous at 25 years.

You want income, not a lump sum. $280,000/year in NOI from a paid-off building is a retirement plan. If your goal is annual cash flow rather than a one-time liquidity event, BTR delivers.

Your tax situation favors rental income over capital gains. Strata sale profits are taxed as business income if CRA determines you’re a builder (which they will, on a purpose-built project). Rental income from a long-term hold is taxed differently — and the building’s depreciation (CCA) provides tax shelter during the hold period.

The Irreversibility Premium

The exit problem is real and permanent. You’re trading optionality for density, financing, and long-term compounding.

That trade-off is excellent for a 55-year-old who owns a paid-off lot and wants retirement income from a building they’ll hold for 25 years.

It’s terrible for a 35-year-old who bought a lot with $400K in equity, plans to hold for 8 years, and might need to liquidate for life changes.

Know which one you are before you commit. The secured rental covenant doesn’t care about your changing circumstances.

David Babakaiff is the Co-Founder and CEO of VanPlex, a Vancouver-based company specializing in multiplex development and Missing Middle housing. VanPlex uses its AI-powered PlexRank system to identify and underwrite multiplex conversion opportunities under BC’s Bill 44 zoning reforms.

Wondering whether BTR or strata is right for your lot? Visit VanPlex.ca and compare both proformas.