Honest Assessment

Risks & Problems with Build-to-Rent Multiplex

This is the page most BTR promoters skip. Every other page on this hub explains how the model works and where it fits. This one explains where it breaks — and why most lots fail the test.

What You Need to Know First

- ✓Secured rental tenure is permanent. You cannot sell units individually. Ever. This is not a risk to manage — it is a structural decision.

- ✓Metro Vancouver purpose-built vacancy hit 3.7% in 2025 — a 30-year high. The "guaranteed demand" story has a crack in it.

- ✓BC caps rent increases at 2.3% for 2026. Your insurance, taxes, and maintenance do not respect that cap.

- ✓Most lots fail the BTR test. That is not a flaw in the analysis. That is the analysis working correctly.

Risk Severity at a Glance

Exit Lock

5/5Permanent. Secured rental tenure eliminates individual unit sales. This is not a risk you manage — it is a structural feature you accept or reject.

Lease-Up Exposure

4/5One vacant unit in a 6-unit building is 16.7% vacancy. Small buildings have no buffer.

Operating Burden

3/5Not passive. Maintenance, tenant turnover, insurance, and property management fees eat 30-40% of gross rental income.

Land Basis Trap

4/5The single most common mistake. Paying strata-justified land prices for a rental hold destroys yield before construction starts.

Policy Uncertainty

3/5DCL waivers are municipal policy. Density bonuses are not legislation. Any underwriting built on assumed incentives is fragile.

Rent Growth Compression

3/5BC caps rent increases at 2.3% for 2026. Your costs rise faster. The math erodes over time unless the initial yield is strong enough.

The Exit Problem

Secured rental tenure means you can never sell units individually. Period. The project becomes a single-title asset that sells at a cap rate discount to strata. On a $3.5M build in Vancouver, the difference between a strata exit and a rental disposition can be $800K or more.

That is not a risk. It is a permanent structural choice baked into a housing agreement registered on title with the City. There is no sunset clause. No conversion mechanism. No council vote that reverses it.

Your buyer pool shrinks from "anyone who wants a home" to "investors who want a stabilized rental building." Those buyers underwrite on cap rate and NOI, not on comparable sale prices. A 6-unit strata project might sell at $4.2M in individual dispositions. The same building as secured rental might trade at $3.4M based on a 4.5% cap.

If you are comfortable never selling individual units, the exit problem is not a problem. It is just a fact. But if you entered rental because someone told you it was "the same thing but with better financing," you were misled.

Lease-Up Risk

One empty unit in a 6-unit building is 16.7% vacancy. In an 8-unit, it is 12.5%. The Debt Coverage Ratio math on a small multiplex is unforgiving. Miss one month's rent on two units during lease-up and your lender is already nervous.

| Building | Vacant | Vacancy % | Gross Rent/mo | Est. NOI/mo | DCR | Status |

|---|---|---|---|---|---|---|

| 6-unit | 0 | 0% | $16,200 | $10,530 | 1.32x | Comfortable |

| 6-unit | 1 | 16.7% | $13,500 | $8,100 | 1.01x | Lender concern |

| 6-unit | 2 | 33.3% | $10,800 | $5,670 | 0.71x | Covenant breach |

| 8-unit | 0 | 0% | $20,800 | $13,520 | 1.35x | Comfortable |

| 8-unit | 1 | 12.5% | $18,200 | $11,375 | 1.14x | Tight |

| 8-unit | 2 | 25% | $15,600 | $9,230 | 0.92x | Covenant breach |

Assumes $2,700/month average rent per unit for 6-unit, $2,600 for 8-unit. 35% operating expense ratio. Monthly debt service of $7,975 (6-unit) and $10,000 (8-unit) based on typical CMHC-insured terms. Your numbers will differ.

Metro Vancouver context: CMHC reported the purpose-built rental vacancy rate in Metro Vancouver hit 3.7% in 2025 — up from 1.6% in 2024 and the highest in 30 years. Provincial population growth is slowing due to declining international migration. The "guaranteed demand" assumption deserves stress testing, not faith.

Operating Burden

Small multiplex is not passive income. Anyone who tells you otherwise has never managed one.

Expense Ratio

Property management fees alone run 6-8% of gross rent. Add insurance increases (up 15-25% annually in BC since 2022), property tax, maintenance reserves, and common-area utilities. The "passive income" story evaporates fast.

Rent Growth Cap

BC ties the maximum allowable rent increase to CPI. In 2026 that is 2.3%, down from 3% in 2025. Your costs do not follow CPI. Insurance, property tax reassessments, and maintenance all outpace that cap. The margin erodes every year unless your starting yield absorbs the compression.

What Nobody Mentions

- ▸Tenant disputes go through the BC Residential Tenancy Branch. Average wait times for a hearing run 8-14 weeks. During that period, a non-paying tenant stays.

- ▸Personal-use eviction in a purpose-built rental building with 5+ units is effectively prohibited under recent BC policy changes. You cannot evict a tenant to move in yourself.

- ▸Turnover in small buildings hits harder. Painting, minor repairs, and vacancy loss on one unit cost the same whether you own 6 units or 60. But in a 6-unit, that turnover represents 16.7% of your revenue, not 1.7%.

- ▸Strata insurance crisis applies to new construction too. Multi-unit wood-frame buildings in BC have seen insurance premiums triple since 2019 in some cases.

The Land Basis Trap

This is the most common mistake. It kills more BTR deals than construction cost overruns, lease-up delays, and policy changes combined.

The math: A lot trades at $2.5M because the strata comparable says it is worth that. Six strata units at $750K each produce a $4.5M gross disposition — the land cost makes sense against that exit. But the owner chooses rental. Now the yield is calculated on a $2.5M land basis plus $2.8M construction cost, and the rental income has to service a $5.3M all-in number. At $2,700/month average rent across 6 units, gross annual rent is $194,400. That is a 3.7% gross yield on cost. After expenses, you are at 2.2-2.5% net.

The rental deal needed a $1.6-1.8M lot to work. The buyer paid $2.5M. That $700K delta is not recoverable through better management, higher rents, or government incentives. The deal was dead at the land purchase.

Rental-Workable Land Basis

$1.4–1.8M

Range where a 6-unit Vancouver rental hold can clear 1.1x DCR with conservative rent assumptions.

Typical R1-1 Land Price

$2.0–2.8M

What most 50-ft Vancouver lots actually trade at. Priced for strata exit, not rental hold.

The Gap

$400K–1M

The amount by which most Vancouver lots are overpriced for rental. This gap is the deal killer.

When BTR Is the Wrong Answer

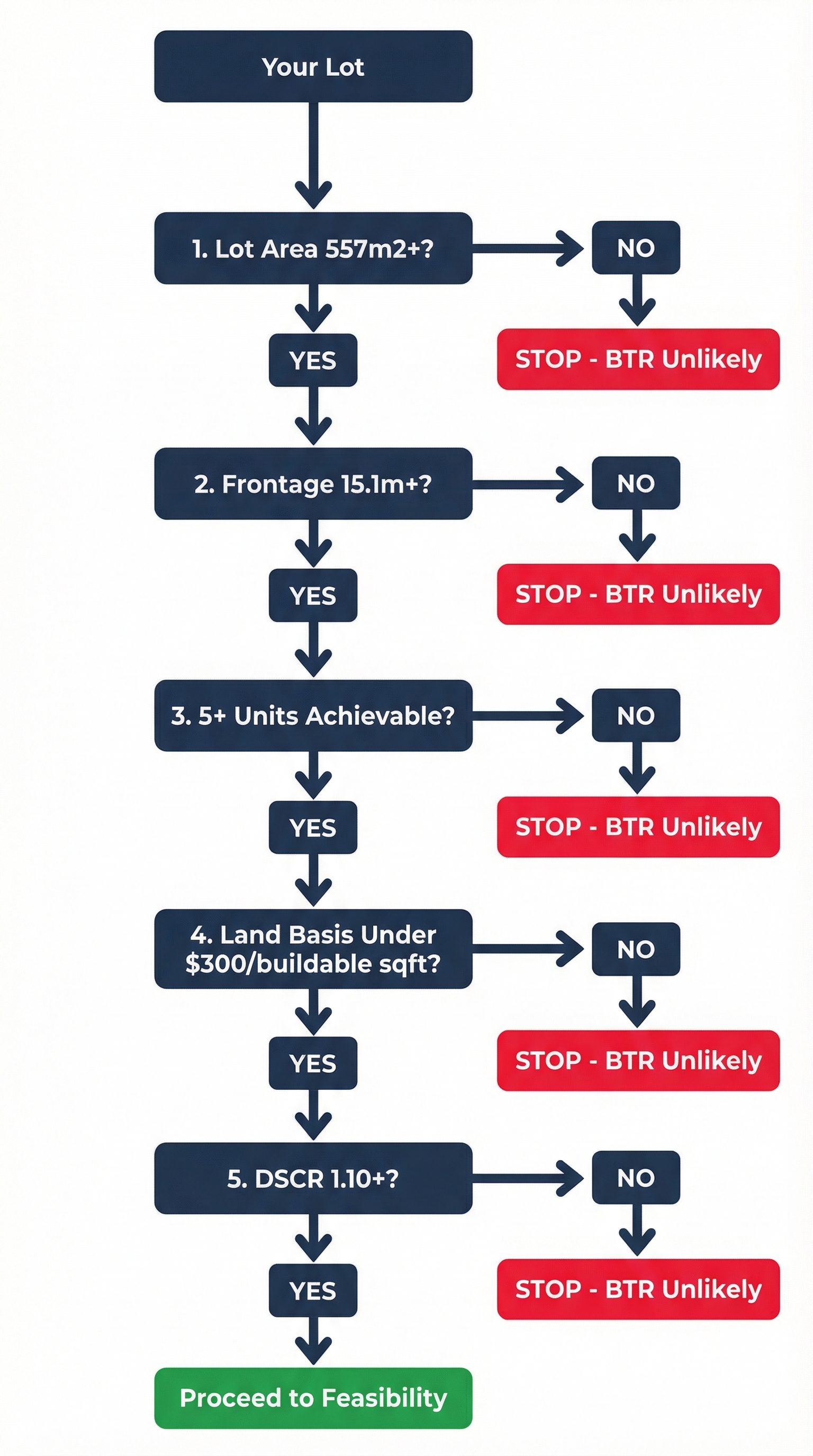

Most lots fail the BTR test. Here are the specific conditions that disqualify a site.

Frontage under 50 feet

You top out at 4 units. The CMHC threshold is 5. The financing advantage disappears and you are left holding a small rental building at strata land cost.

Fewer than 5 achievable units

Without clearing the 5-unit threshold, MLI Select is off the table. Conventional financing on a 4-unit rental building means shorter amortization, higher rates, and tighter DCR.

Land cost exceeds what rental income can service at 1.1x DCR

Run the math backwards. If the stabilized rent roll cannot service the debt at a 1.1x coverage ratio based on your all-in cost, rental does not work on that lot. Full stop.

No rental-specific incentives in that municipality

Vancouver offers DCL waivers and density bonuses for secured rental. Richmond does not. Surrey does not. If the municipality treats rental and strata identically on fees and density, the rental path has no structural advantage — only structural constraints.

The owner needs capital back within 5 years

Secured rental is a hold strategy. Construction takes 18-24 months. Lease-up takes 3-6 months. Stabilization takes another 6-12 months. Refinancing after that. If you need your equity recycled fast, strata is the answer.

Fee and Policy Uncertainty

DCL Waivers

Vancouver's current rental development relief program runs February 2026 to December 2027. It includes full DCL waivers on the residential portion of qualifying secured rental projects. That is a council resolution, not legislation.

A new council, a fiscal crunch, or a policy review can modify or eliminate it. If your pro forma depends on a DCL waiver that has not been confirmed in a rezoning approval, you are underwriting on sand.

Density Bonuses

The jump from 6 strata units to 8 secured rental units in Vancouver R1-1 zones is a density bonus embedded in zoning policy. It is not provincial law. Bill 44 mandates that municipalities allow small-scale multi-unit housing, but it does not mandate specific rental bonuses.

Any underwriting that relies on a rental density bonus should verify the specific bylaw language, not assume it from a summary. Municipal policy can shift with a single council vote.

CMHC Program Risk

CMHC updated MLI Select premiums effective July 14, 2025. A 0.25% surcharge now applies for every 5-year amortization increment above 25 years. A project using 50-year amortization pays an additional 1.25% in premium surcharges. These terms changed once. They can change again.

CMHC has insured over 1.5 million purpose-built rental units in the last decade, including over 340,000 new construction units. The program is not going away. But the specific terms — premium rates, scoring thresholds, amortization limits — are CMHC's to adjust. Do not build a 30-year hold thesis on today's program parameters.

Best For

- ✓ People who have read everything above and still see a path — because the land basis is low enough, the rent roll clears DCR at conservative assumptions, and the hold timeline is genuinely long.

- ✓ Owners who already own the lot and paid well below current market, eliminating the land basis trap entirely.

- ✓ Projects in Vancouver where DCL waivers and the 8-unit rental density bonus have been confirmed at the specific parcel level, not assumed from general policy.

Usually Fails When

- ✕ The land was purchased at strata pricing and the owner pivoted to rental after the fact.

- ✕ The pro forma requires 100% occupancy at market-top rents to clear a 1.1x DCR.

- ✕ The owner has not stress-tested vacancy at 5%, operating expenses at 40%, and rent growth at 2% against real debt service numbers.

- ✕ The timeline requires capital back within 5 years.

What To Verify Before Spending Money

- → Run the DCR math backwards from your actual debt service to find the rent and vacancy you need — then check if that is realistic for your neighbourhood.

- → Confirm whether your municipality offers any rental-specific incentives. Most do not.

- → Get a written confirmation of DCL waiver eligibility from the City before committing to secured rental tenure.

- → Talk to a BC-licensed property manager about actual operating costs for a new 6-8 unit building before using generic expense ratios.

Frequently Asked Questions

Can I convert a secured rental project back to strata later?

What happens if Metro Vancouver vacancy rates keep rising?

How much does one vacant unit actually affect debt coverage?

Is the rent increase cap really a problem for BTR?

Are DCL waivers for secured rental guaranteed?

What is the biggest single mistake people make with BTR multiplex?

Related Reading

When Build-to-Rent Doesn't Work: 7 Lots That Failed the Test

Real examples of lots that looked viable but failed on land basis, unit count, or financing thresholds.

The Exit Problem: You Can Never Sell Units Individually

The permanent structural constraint of secured rental tenure and what it means for your disposition strategy.

Lease-Up Risk on a Small Multiplex: Why One Empty Unit Hurts

The DCR math on a 6-unit building is unforgiving. One vacant unit can push you to lender concern territory.

Most BC Lots Fail the Build-to-Rent Test. Here's How to Screen Yours

A five-filter screening process to identify which lots actually support a rental hold before you commit.

Official Sources Referenced

Screen Your Lot for Build-to-Rent

Enter any BC address to compare rental hold potential, unit count, and the for-sale alternative before you spend money on drawings.