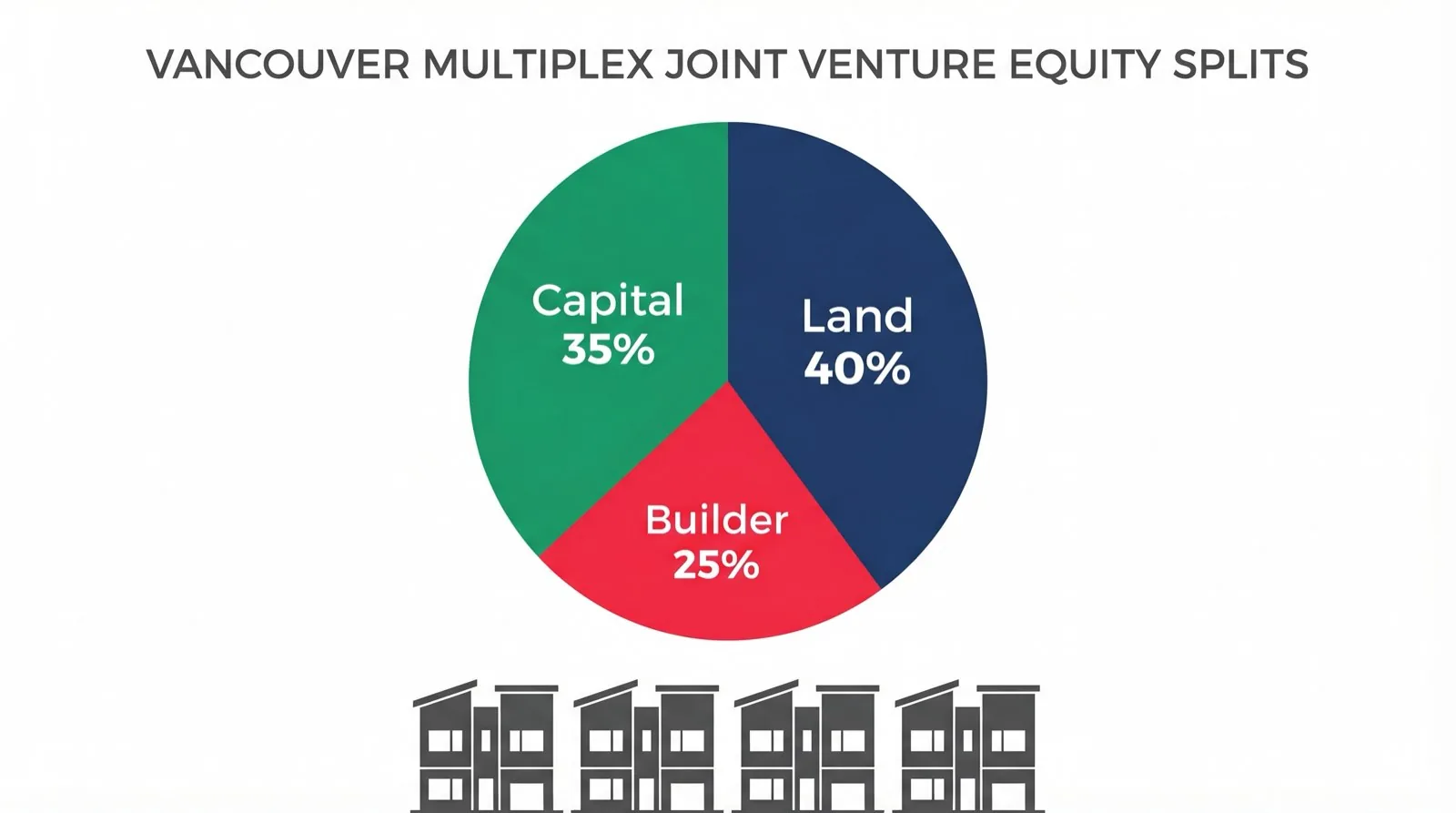

In 2024, the average Vancouver multiplex deal needed three things: a multiplex-eligible lot, $2.5–4M of capital, and a credible builder. Almost no single party in BC has all three. That gap is why the joint venture has quietly become the dominant structure for small-lot multiplex development across British Columbia.

This is the working manual.

What a multiplex JV actually is

A multiplex joint venture is a formal partnership between two or more parties — usually a landowner, a capital partner, and a builder or developer — to develop a multi-unit residential building on one or more lots. Each side contributes something different. Each side gets a share of the upside. And the JV agreement is the entire game.

The structure varies. In BC, multiplex JVs are usually held through one of four legal forms:

- Bare trust — a trustee holds legal title for the beneficial owners. Common for pre-construction holds because beneficial interest can be transferred without triggering property transfer tax.

- General partnership — partners share profits, losses, and unlimited joint liability. Simple but exposes everyone to everything.

- Limited partnership — a general partner runs the project, limited partners contribute capital and are shielded from liability beyond their cheques. The default for deals with passive money.

- Co-ownership / TIC — each party holds a fractional undivided interest on title. Workable for two-party family deals but lenders dislike the partition exposure.

Pick the wrong one and you eat unnecessary tax, take on unnecessary liability, or watch your lender walk. Pick the right one and the structure becomes invisible — exactly the goal.

The three roles

Almost every BC multiplex JV reduces to three archetypes:

Landowner

Brings the lot, usually contributed at appraised value. Expects a percentage of the project proportional to the land value plus a piece of the upside above pref. Carries the risk that the lot is contributed early in the timeline — if the deal fails, the lot goes through the JV waterfall like any other asset.

The single biggest mistake landowners make is undervaluing their contribution. A 33-foot Vancouver lot that supports a 6-plex is not worth its 2019 assessed value. It is worth what a builder would pay for the right to build there today, with the new density unlocked. Get an independent appraisal before any conversation.

Capital partner

Brings cash, usually called in tranches as the project progresses. Expects a preferred return (commonly 8% in BC multiplex deals) before any sponsor or builder profit, plus a proportional share of upside above pref.

The mistake capital partners make is treating multiplex JVs like passive bonds. They are not. Capital calls are real. Default remedies are real. If the sponsor goes silent, the capital partner needs to know how to enforce reporting. Get the major-decision veto, the audit right, and the buy-out trigger if the sponsor is removed for cause.

Builder / sponsor

Brings construction capacity, project management, the GC license, and often the deal itself. Expects market-rate GC fees plus carried interest above the preferred return. Carries personal guarantees on the construction loan and reputation if the deal fails.

The mistake builders make is treating the JV like a fee-for-service gig with a small equity tip. The whole point of climbing into a JV structure is to compound — to use one successful project to source the next, and the next, until you are the developer rather than the contractor.

How the capital stack actually works

A typical Vancouver 6-plex JV with a $2.0M lot and $2.4M of hard costs has a capital stack that looks roughly like this:

- Senior construction loan ($3.3M, 75% of cost — or 95% if CMHC MLI Select qualifies)

- Land contribution ($2.0M, contributed by the landowner at appraised value)

- Capital partner equity ($0.8M, called in tranches: closing, permits, construction draws, lease-up reserve)

- Sponsor / builder equity ($0.3M, often deferred fees plus a small cash contribution)

Total capital stack: $6.4M against a project of similar gross value. The leverage and the cost discipline are what make the deal work.

When CMHC MLI Select is reachable — five or more units, purpose-built rental, credible operator — the senior loan can stretch to 95% of cost, dramatically reducing the equity requirement and opening the deal to smaller capital partners.

The waterfall is the whole game

People obsess over the equity split. Is it 50/50 or 60/40? They should be obsessing over the waterfall.

A standard four-tier multiplex JV waterfall looks like:

- Return of capital — first distributions go to repaying contributed capital, pro-rata to contributors.

- Preferred return — capital then earns its pref (commonly 8% IRR) before any profit goes to the sponsor or builder.

- Catch-up — once pref is paid, the sponsor “catches up” on promote at a 50/50 or 100% split until the sponsor has reached their share of pref-level profits.

- Promote — all remaining profit splits 70/30 or 80/20 (capital / sponsor), depending on deal difficulty and sponsor leverage.

Two deals can have identical 50/50 equity splits and produce wildly different take-home amounts depending on the waterfall. A $1.2M profit on the same project might pay the capital partner $660,800 under one waterfall and $480,000 under another. The sentences in the waterfall section are worth more than the percentage on the cap table.

Where multiplex JVs go wrong

We have seen the same six failures over and over:

- Cost overruns. Construction comes in 15% over budget. The sponsor calls additional capital. The capital partner refuses or cannot fund. Default remedies kick in, and someone gets diluted.

- Scope creep. The sponsor upgrades finishes mid-project without consent. Other partners see this as a unilateral spend decision and refuse to fund it.

- Unpaid capital calls. A capital partner misses a tranche. The other partners now have to either dilute the defaulter or fund the gap themselves.

- Related-party vendor markup. The builder partner uses a related-party trade and the markup exceeds market rates. Other partners discover this through an invoice audit.

- Refinance disagreement. At stabilization, the sponsor wants to refinance and hold; the capital partner wants to sell and exit. The agreement says both are allowed.

- Death or incapacity of a partner. Mid-project, a partner dies. Their interest passes to an estate that has no relationship with the other partners.

Every one of these is preventable in the agreement. The mistake is assuming the worst case will not happen to you.

What to negotiate before you sign

If you are a landowner contributing land, fight for:

- Land contributed at independent appraised value, with a written valuation memo

- A floor on your ownership percentage that survives dilution events

- Right of first refusal if any other partner tries to sell their interest

- An independent project monitor (not the builder partner)

- A cap on related-party vendor contracts

- A veto on related-party GC contracts above a stated threshold

If you are a capital partner, fight for:

- Preferred return paid before any sponsor or builder profit

- Major-decision veto on sale, refinance, scope change, additional capital

- An independent quantity surveyor reviewing monthly draws

- A cap on related-party fees

- Quarterly reporting with construction draw schedule and variance to budget

- A buy-out right if the sponsor is removed for cause

If you are a builder, fight for:

- Market-rate GC fees, not deferred fees you may never see

- A guaranteed maximum price contract, not open-ended cost-plus

- Reasonable promote above the pref hurdle

- Personal guarantee allocation that is reciprocal where possible

The honest decision

A JV is not always the right answer. For some lots, selling outright is faster and cleaner. For others, self-developing without partners is more profitable. The JV becomes interesting only when you cannot do the deal alone, and the deal is good enough to justify bringing in partners.

For a Vancouver landowner with a $2M lot and $400k of savings, a JV is often the only way to keep the upside. For a builder with three completed multiplexes and a network of capital, a JV is the path from fee-for-service into carried interest. For a passive investor with $500k looking for multiplex exposure, a JV is the only way in without becoming a developer.

Read the How It Works, the JV Agreements, and the Profit Waterfalls pages before any conversation with a lawyer. Bring real questions. Then sign with your eyes open.

The full hub lives at /joint-venture.