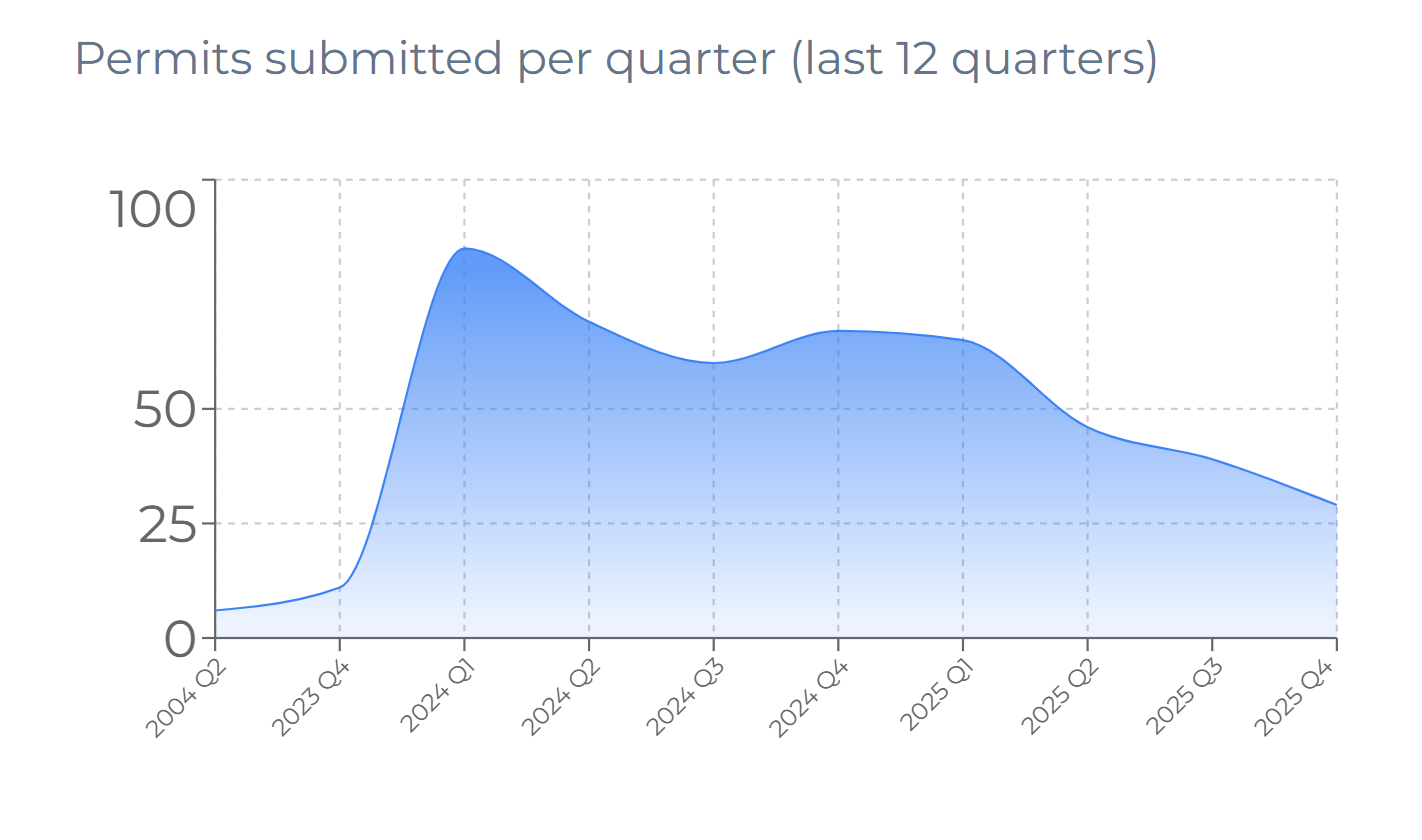

Vancouver multiplex permits spiked when zoning changes came through in 2024-2025—then started declining. Over the past year, quarterly submissions have trended steadily downward. This isn’t a sign multiplex is “dead.” It’s the market reaching the same conclusion many developers have: zoning capacity isn’t the same as feasibility.

TL;DR (Key Takeaways)

- Permit submissions peaked after zoning changes, then declined steadily through 2025

- The gap between what’s allowed and what pencils is where projects quietly fall away

- Construction costs haven’t compressed; land prices haven’t reset

- Missing-middle buyers behave differently than single-family buyers

- Projects that still work share specific characteristics: geometry, absorption-aligned sizing, execution speed, margin buffer

- 2026 is about selectivity, not enthusiasm—identifying the profitable, repeatable sliver

The Surge Already Happened

When the zoning changes came through, permits spiked quickly. That made sense. Rules changed, and people moved fast to test them.

What’s more interesting is what happened after.

Even before sales softened meaningfully, permit submissions started declining. Over the past year they’ve been trending down quarter over quarter.

To see this chart and other permit stats, visit VanPlex Permits

That doesn’t mean multiplex development is over. It does suggest the easy assumptions didn’t hold for very long:

- Buying lots under market value — Competition pushed prices up

- Over-optimistic profit projections — Reality set in when construction bids arrived

- Ignoring taxable change-of-use consequences — Homeowners discovered unexpected tax bills

- Marginal math, but did it anyway — Projects that barely worked on paper failed in practice

The permit curve is the market slowly processing this information.

Zoning Capacity Isn’t Feasibility

Across Vancouver, Burnaby, the City of North Vancouver, and Kelowna, the same pattern emerges.

You can often build more square footage than before. But once you price construction ($400-500/sqft), financing (7-9% construction loans), and realistic sale prices, a lot of sites don’t land where people expected.

| Factor | Expectation | Reality |

|---|---|---|

| Land Prices | Would reset lower | Stayed elevated |

| Construction Costs | Would compress with volume | $400-500/sqft persists |

| Buyer Demand | Same as single-family | Missing-middle buyers behave differently |

| Absorption | Quick sales at premium | Longer timelines, price sensitivity |

| Profit Margins | 20-30% | Many projects at 5-10% or negative |

Missing-middle in this context means the housing stock priced between a house in your neighborhood and a condo—ground-oriented homes for families priced out of detached but wanting more than a high-rise unit.

These buyers are price-sensitive. They comparison-shop. They don’t pay the same premium per square foot as single-family buyers.

So the constraint shows up in the numbers, not the bylaws. That gap between what’s allowed and what pencils is where a lot of projects quietly fall away.

What Separates Projects That Still Work

The projects that still make sense tend to share a few characteristics:

Lots with Specific Geometry

Not every eligible lot is a good lot. The ones that work have:

- Efficient dimensions for unit layout (minimize wasted circulation)

- Favorable orientation for light and views

- Minimal servicing complications

- No easements, covenants, or encumbrances eating into buildable area

Building Sizes Aligned to Buyer Absorption

Chasing maximum zoning doesn’t maximize profit. The winning projects:

- Build to what buyers actually want, not what’s permitted

- Right-size units for the target market (1,200-1,400 sqft sweet spot for families)

- Don’t over-finish or under-finish relative to neighborhood expectations

Execution Models Built for Speed and Repetition

Time is money when you’re carrying construction financing at 8%+. Projects that work:

- Use standardized, pre-approved designs where possible

- Have consultant teams that know the permit process

- Move from approval to completion in 12-18 months, not 24-30

Enough Margin to Survive Variability

Markets shift. Costs creep. Sales take longer than projected. Successful projects:

- Build in 15-20% contingency

- Don’t require perfect conditions to break even

- Can absorb a 5-10% price correction and still deliver returns

These conditions exist, but they’re not evenly distributed. And they’re not obvious without doing the work at scale.

What This Means for Investors in 2026

If you’re thinking about multiplex as a category, this is the phase where selectivity starts to matter more than enthusiasm.

The next cycle isn’t about chasing every eligible lot. It’s about understanding which combinations of land, design, and delivery actually hold up when conditions change.

Boring and predictable beats exciting and risky.

The permit curve reflects the market reaching this conclusion. The sites that continue to attract permit applications are the ones where the math actually works—not the ones where optimism filled the gaps.

The 2026 Lens

Going into 2026, the focus shifts to:

- Identifying the profitable sliver — Not “which sites allow multiplex” but “which ones work under conservative assumptions”

- Execution discipline — Speed, cost control, and standardization

- Realistic absorption — Building for actual buyer behavior, not theoretical demand

- Margin protection — Enough buffer to survive market noise

What’s Coming: PlexReady Scores

2026 will be about positioning for the truly profitable, repeatable multiplex opportunities. The constraint isn’t zoning anymore—it’s identifying which lots actually work.

We’re developing a PlexReady score that identifies exactly these opportunities: the sites where geometry, costs, and market align to produce reliable returns.

The constraint will be accessing that limited capacity.

If you’re thinking about this space the same way—focused on what actually pencils rather than what’s theoretically possible—check your property’s potential or reach out directly.

Happy New Year,

David Varadi Founder, VanPlex

PlexRank | Profit with Multiplex