Multiplex Is Not Multifamily

Investors Who Treat It That Way Are Benchmarking Against the Wrong Comparables.

A framework for understanding BC’s newest real estate asset class on its own terms: capital mechanics, risk architecture, and the structural Alpha most investors are missing.

Investors hear “multiplex development” and mentally file it next to multifamily apartment buildings, or worse, next to a duplex flip. They apply the same underwriting framework, the same capital structure logic, the same return expectations. Then they benchmark the outcome against the wrong comparables and wonder why the strategy does not resolve cleanly.

The problem is not the numbers. The problem is the category.

Multiplex programmatic development is a distinct strategic asset class. It has its own capital mechanics, its own risk architecture, and its own Alpha engine. Evaluating it on the terms of conventional multifamily is to misread the instrument entirely.

What Makes an Asset Class?

To warrant treatment as a distinct asset class, a strategy must satisfy three conditions: a risk and return profile that cannot be replicated by other strategies, structural characteristics requiring dedicated underwriting frameworks, and Alpha generated through mechanisms unique to its category.

Programmatic multiplex development satisfies all three. The following sections address each in turn.

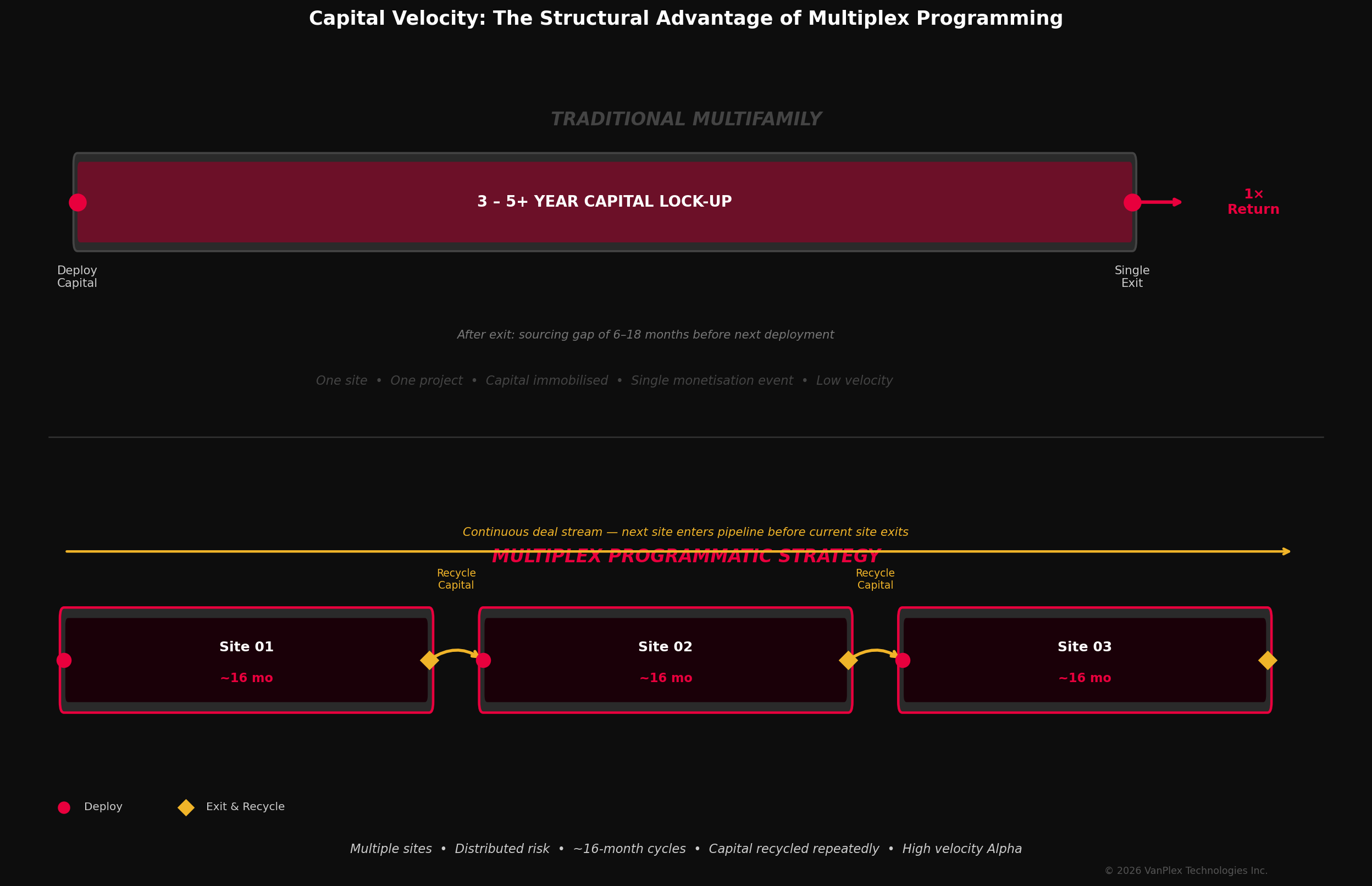

1. Capital Velocity as the Primary Return Driver

The most fundamental distinction between programmatic multiplex development and conventional multifamily investment is not scale, product type, or geography. It is capital velocity: the rate at which invested equity completes a full deployment and return cycle.

Traditional multifamily development is characterized by long-duration capital exposure. Equity is committed for three to five years encompassing entitlement, construction, stabilization, and exit. Capital completes a single return cycle over that horizon. And crucially, when that cycle ends, the operator must start the sourcing process again from scratch. In practice, investors in multifamily programs routinely face gaps of 6 to 18 months between the exit of one project and full deployment into the next. Capital sits idle. Return clock stops. Compounding pauses.

Programmatic multiplex development operates under an entirely different capital dynamic. Because sites are smaller and process timelines are compressed into approximately 16 months, new sites can be entering the pipeline continuously while existing sites are mid-construction or presale. Capital is never idle. The next deployment is already underway before the current one exits. This is a structural feature of the strategy.

The relevant evaluation metric is therefore not simply project-level IRR, but capital productivity: the amount of return generated per unit of time per dollar deployed. Strategies that increase deployment frequency without proportionally increasing risk can outperform longer-duration alternatives even when individual project returns appear comparable.

Figure 1: Capital Velocity. Traditional Multifamily vs. Multiplex Programmatic Strategy | © 2026 VanPlex Technologies Inc.

Figure 1: Capital Velocity. Traditional Multifamily vs. Multiplex Programmatic Strategy | © 2026 VanPlex Technologies Inc.

The After-Tax Comparison

The table below applies BC combined corporate tax (27%) to profits at each exit event for both strategies. Multifamily tax is applied once at the single terminal exit. Multiplex tax is applied at each of the three cycle exits before capital is reinvested. The 60% ROE per 16-month multiplex cycle reflects the return profile of PlexRank-eligible properties. Multifamily IRR range of 15-20% reflects the published industry hurdle rate for wood-frame and concrete-podium midrise condo development in Canada.

Traditional Multifamily — Industry IRR Hurdle Range

| Strategy | Timeline | Tax Events | Net Return on $1M | Net Cumulative ROE |

|---|---|---|---|---|

| Multifamily — 15% IRR (hurdle minimum) | 48 months, 1 exit | Once at exit | $547,000 | 55% |

| Multifamily — 20% IRR (hurdle midpoint) | 48 months, 1 exit | Once at exit | $784,000 | 78% |

Multiplex Programmatic — 60% ROE Per 16-Month Cycle

| Cycle | Capital In | Gross ROE | Tax | Capital Forward |

|---|---|---|---|---|

| Cycle 1 (months 1-16) | $1,000,000 | 60% | $162,000 | $1,438,000 |

| Cycle 2 (months 17-32) | $1,438,000 | 60% | $233,000 | $2,068,000 |

| Cycle 3 (months 33-48) | $2,068,000 | 60% | $335,000 | $2,974,000 |

| 3-Cycle Total | 48 months | 3 tax events | $1,974,000 net (197% ROE) |

Three recycled 16-month cycles at 60% ROE per cycle, taxed at BC corporate rates at each exit, yields a net cumulative return of 197% on the original capital over 48 months.

The same capital deployed into a multifamily project at the industry’s own hurdle rate of 15-20% annualized IRR over the same 48 months, taxed once at terminal exit, returns 55-78% net. Same timeframe. Same tax regime. Entirely different outcome. Capital velocity is the variable.

The 60% ROE per cycle assumption reflects the return profile of properties identified through VanPlex’s PlexRank screening at the right tail of the Vancouver distribution. PlexRank provides deal flow certainty at these return levels by systematically identifying qualifying properties before acquisition. It is not the median market outcome.

2. Layers of Capital: The Stack Is Different

Traditional multifamily operates with a capital stack institutional investors know well: senior construction debt, mezzanine or preferred equity, and GP/LP equity at the base. The stack is deep because the project is large, the timeline is long, and the risk profile demands multiple layers of cushion.

Programmatic multiplex runs a fundamentally different stack: shallower, faster-turning, and structurally dependent on the land position of each site. The configuration varies materially based on how a site is acquired. There are three primary scenarios:

| Land Position | Capital Structure | Key Characteristic |

|---|---|---|

| A: Land owner, no mortgage | Co-development agreement. No equity required beyond land contribution. Senior construction debt only. Profits split at completion. | Highest equity efficiency for both parties. Simplest stack. |

| B: Land owner, partial mortgage | GP/LP equity or preferred equity retires existing mortgage at project outset. Creates clean senior construction loan. Land owner retains participating equity stake. | Clears encumbrance. Creates aligned LP participation without a full acquisition. |

| C: Full acquisition via MLS | 100% of purchase price funded by equity (GP/LP or investor capital). Senior construction debt funds the build. Two-tier stack. | Reserved exclusively for properties where PlexRank confirms 100%+ ROE at acquisition basis. |

Scenario A represents the highest-efficiency deployment available in the BC market today. A landowner with no encumbrance becomes a co-development partner, contributing land value against the developer’s construction management and capital access. Senior debt funds the build. Profits split at completion. No mezzanine. No acquisition cost. Maximum equity efficiency for both parties.

Scenario B is the most common structure in today’s market. A landowner carrying a partial mortgage can be brought into the program by deploying preferred equity or GP/LP capital to retire the encumbrance at project outset. This clears the debt, creates a clean senior construction loan, and converts the landowner from a motivated seller into a participating equity partner with aligned incentives.

Scenario C is reserved for acquisitions where PlexRank confirms 100% or greater ROE at the proposed acquisition basis. Buying at full market value on the open market only makes sense when the return profile is exceptional and verifiable before commitment. That discipline is what makes the program defensible at scale.

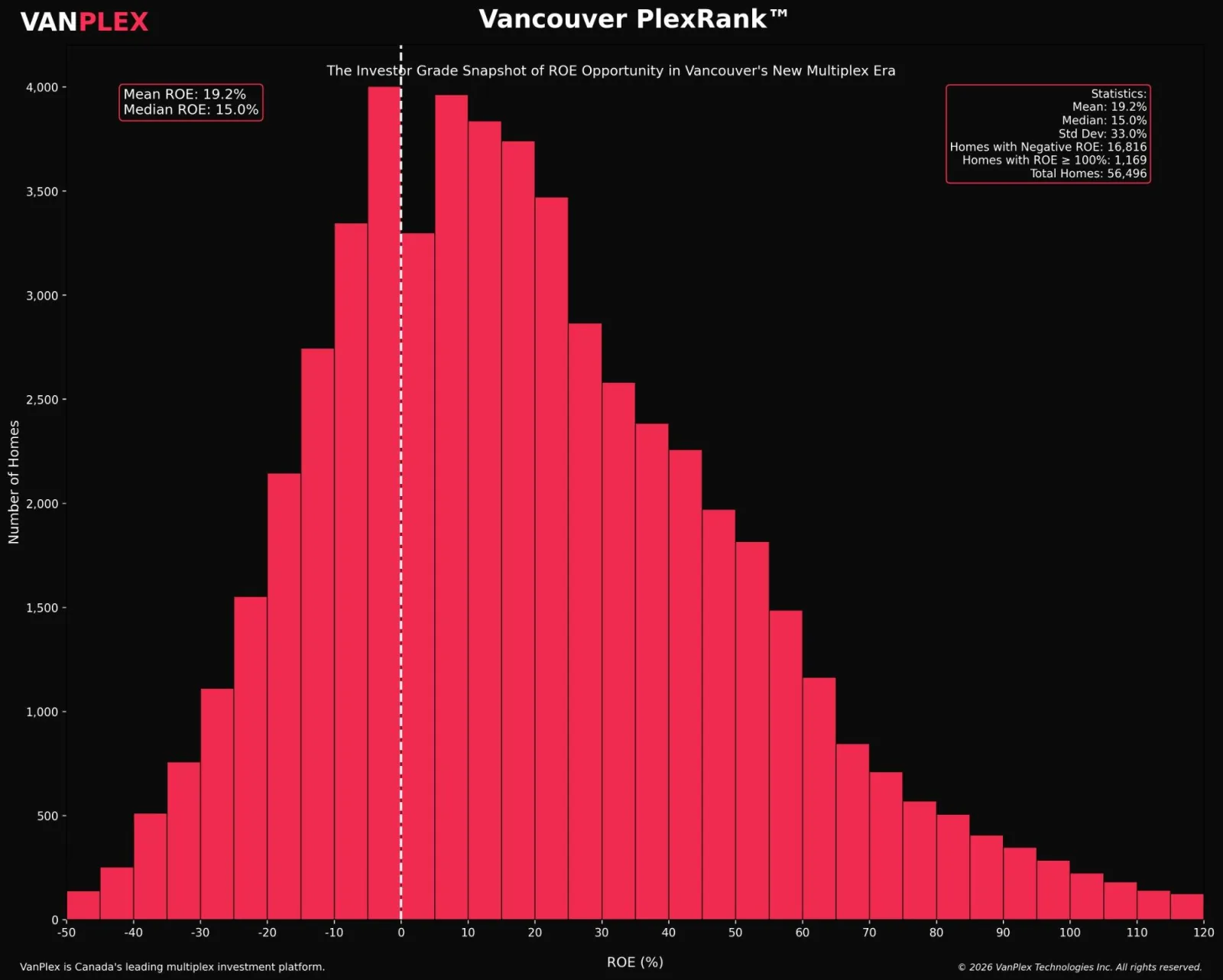

3. Starting on the Right Side of the Distribution

Most investors approach multiplex development by evaluating properties reactively and accepting whatever distribution of outcomes the market presents. PlexRank inverts this.

Our Q1 2026 analysis of 56,496 sample R1-1 zoned properties across Vancouver reveals a wide ROE distribution, from deeply negative outcomes on the left tail to 100% or greater ROE properties on the right. The mean is 19.2%. The median is 15.0%. But the shape of the distribution is the real insight.

Figure 2: Vancouver PlexRank ROE Distribution Across 56,496 Eligible Properties | Q1 2026 | © 2026 VanPlex Technologies Inc.

Figure 2: Vancouver PlexRank ROE Distribution Across 56,496 Eligible Properties | Q1 2026 | © 2026 VanPlex Technologies Inc.

1,169 properties in Vancouver sit at or above 100% ROE. These are not discovered by intuition or realtor relationships. They are identified through systematic analysis of lot dimensions, FSR entitlement, construction cost basis, and neighbourhood sale comps applied against a defined acquisition price. PlexRank was built specifically to locate these properties before they are acquired, and in fact many of them are on MLS.

A programmatic multiplex strategy does not have to accept the average outcome of the market. It can elect to operate exclusively on the right side of the distribution, targeting only properties where ROE clears 100% at acquisition. This is a risk management decision as much as a return decision.

The practical consequence: a program that screens every acquisition through PlexRank before deploying capital is not running the same risk profile as a developer acquiring opportunistically. It is operating with a defined entry filter that systematically eliminates the left tail of the distribution before any commitment is made.

4. Distributed Risk vs. Concentrated Risk

Conventional multifamily concentrates capital into a single entitlement path, a single construction timeline, and a single absorption event. The risk profile is binary at each stage. A permit delay, a cost overrun, lack of pre-sales, or softening absorption at the wrong moment impairs the entire project.

Programmatic multiplex distributes capital across multiple smaller, sequential risk events. Variance on any single site does not impair the program. Portfolio mathematics replaces binary outcome risk.

| Risk Factor | Concentrated (Multifamily) | Distributed (Multiplex Program) |

|---|---|---|

| Capital concentration | 100% in one entitlement | Distributed across 3 to 10 sites |

| Entitlement risk | Single permit path, binary outcome | Multiple parallel permit processes |

| Absorption risk | One selldown event, one market window | Sequential exits across multiple market windows |

| Construction overrun | Impairs entire project return | Contained to one site, program continues |

| Time horizon | 3 to 5 years locked | 16-month rolling process cycles, capital never idle |

| Correction exposure | Full capital at risk across a 4-year horizon | Sub-16-month exposure per deployment |

The critical insight is that exposure to any single risk event is contained. A 10% cost overrun on Site 02 does not affect Site 01’s already-realized return or Site 03’s construction timeline. The program absorbs site-level variance the way a diversified portfolio absorbs individual position risk: through distribution, not concentration.

5. The Alpha Is Structural, Not Cyclical

In multifamily development, Alpha comes primarily from two sources: timing the market correctly and identifying underpriced land. Both are cyclical bets. Get the cycle wrong, or miss on land basis, and returns compress sharply.

Multiplex programmatic Alpha has a different origin. It is generated by three structural factors that exist independently of market timing:

Policy Arbitrage — BC’s Bill 44 upzoning created a permanent structural change to land value for eligible lots. The uplift from single-family to 4 to 6 unit entitlement is baked into the land basis of every eligible property in the province. This is not a temporary window. Investors who systematically access this uplift across multiple sites are extracting a policy-created premium that did not exist three years ago.

Cycle Compression — Each 16-month process cycle is a contained risk event. The capital is not exposed to a 4-year macro horizon. The probability of a market correction materially eroding return is structurally smaller because the capital is simply not in the ground long enough for most correction scenarios to fully develop.

Execution Premium — At 4 to 6 units per site, the margin between an average operator and a disciplined one is significant. Permitting speed, construction sequencing, unit mix optimization, and sales strategy each compound across a multi-site program. In large multifamily, these factors are noise. In programmatic multiplex, they are the primary driver of return differentiation.

6. Some Investors Treat Multiplex Like a Duplex Flip

The most common failure mode I observe is investors trying to force multiplex to behave like a duplex build-flip.

The duplex flip model is transactional by nature. Buy a lot, build two units as fast as possible, sell both, bank the spread. Each deal stands alone. Capital is deployed and recovered discretely, with no structural connection between transactions. And because each duplex is effectively a one-off, it tends toward inefficiency: a custom build with custom decisions on every variable, from design to trades selection to unit mix. No two are the same. Nothing compounds.

Applied to multiplex, this on-off model destroys the structural advantages of the asset class. It strips out the programmatic compounding. It ignores capital stack optimization. And critically, it eliminates the execution premium that programmatic repetition creates. When you build the same 6-unit typology across ten sites, you are not building ten custom projects. You are refining a repeatable system. Permitting becomes predictable. Trade pricing improves with volume. Design variables are reduced. Each iteration produces better margins than the last. The on-off duplex model has no access to any of this.

The programmatic multiplex thesis only works at program scale.

A single site is a project. Three sites with recycling capital is a strategy. Ten sites with a systematized pipeline is an asset class with institutional-grade return characteristics. The Alpha is in the repetition and the system, not in any individual transaction.

The investors who will capture the most value from BC’s multiplex era are not the ones who execute one project well. They are the ones who build the operational capacity to run a continuous pipeline: acquiring, permitting, constructing, and selling in a rolling sequence that keeps capital deployed and compounding at all times.

What This Means for Your Portfolio

Multiplex programmatic development offers something genuinely rare in Canadian real estate today: a structural Alpha source that is policy-created, execution-enhanced, and largely inaccessible to institutional capital because of scale constraints. The sweet spot — 4 to 6 units, 16-month process cycles, Lower Mainland land basis — is too small for institutions and too sophisticated for most retail investors and custom builders.

That gap is where the opportunity lives.

In future issues, we will break down site selection filters, underwriting frameworks, capital structuring models for each scenario, and the operational systems that allow a program to scale. If this framework resonates, the analysis runs deeper.