VANPLEX FIELD NOTES — Saturday, May 23, 2026 — Issue No. 008

Most Saturdays before 7 AM Pacific, I share something I’ve been watching, measuring, or building. You’re getting this as an insider who registered for possible investment at vanplex.ca/investor.

For seven issues I’ve made an argument. Bill 44 opened a one-way door, the land hasn’t repriced, the gap is real and measurable. If you’ve read along, you probably believe it by now.

But believing it has paid you exactly nothing.

A thesis is an opinion about the future. A position is money in the ground. The two feel similar on a Saturday morning, but everyone who “knew” Bill 44 mattered in 2023 and did nothing is, financially, indistinguishable from someone who never heard of it.

So this week, no argument. I took a property sitting on MLS right now and ran it all the way through our underwriting to show you the difference between believing the thesis and pricing an actual position.

A listing anyone can see, priced the way we see it

A 50-foot lot on Vancouver’s West Side. Built 1926, R1-1, five units, ~7,465 buildable square feet. PlexRank scored it 10 of 10 — a Signature tier. I haven’t made an offer on it. I underwrote it. Here’s what a deal structured like this would hand a limited partner over a 20-month build-to-sell:

| Illustrative LP economics | |

|---|---|

| LP equity (funds land + closing) | $2,565,500 |

| Preferred return | 9% |

| Profit split above the pref | 60% LP / 40% GP |

| Equity multiple | 1.59x |

| Cash-on-cash | 59.3% over 20 months |

| Annualised | ~35.6% / year |

| Target IRR | 42–46% |

Illustrative of how a deal like this would be structured — not an offer.

The structure is plain: equity goes in as the land, a senior construction loan funds the build, and when the units sell the loan is repaid first, then equity comes back, then the 9% preferred return — and only then is profit split 60/40. The investor sits ahead of the promote, not behind it.

Now let’s try to break it

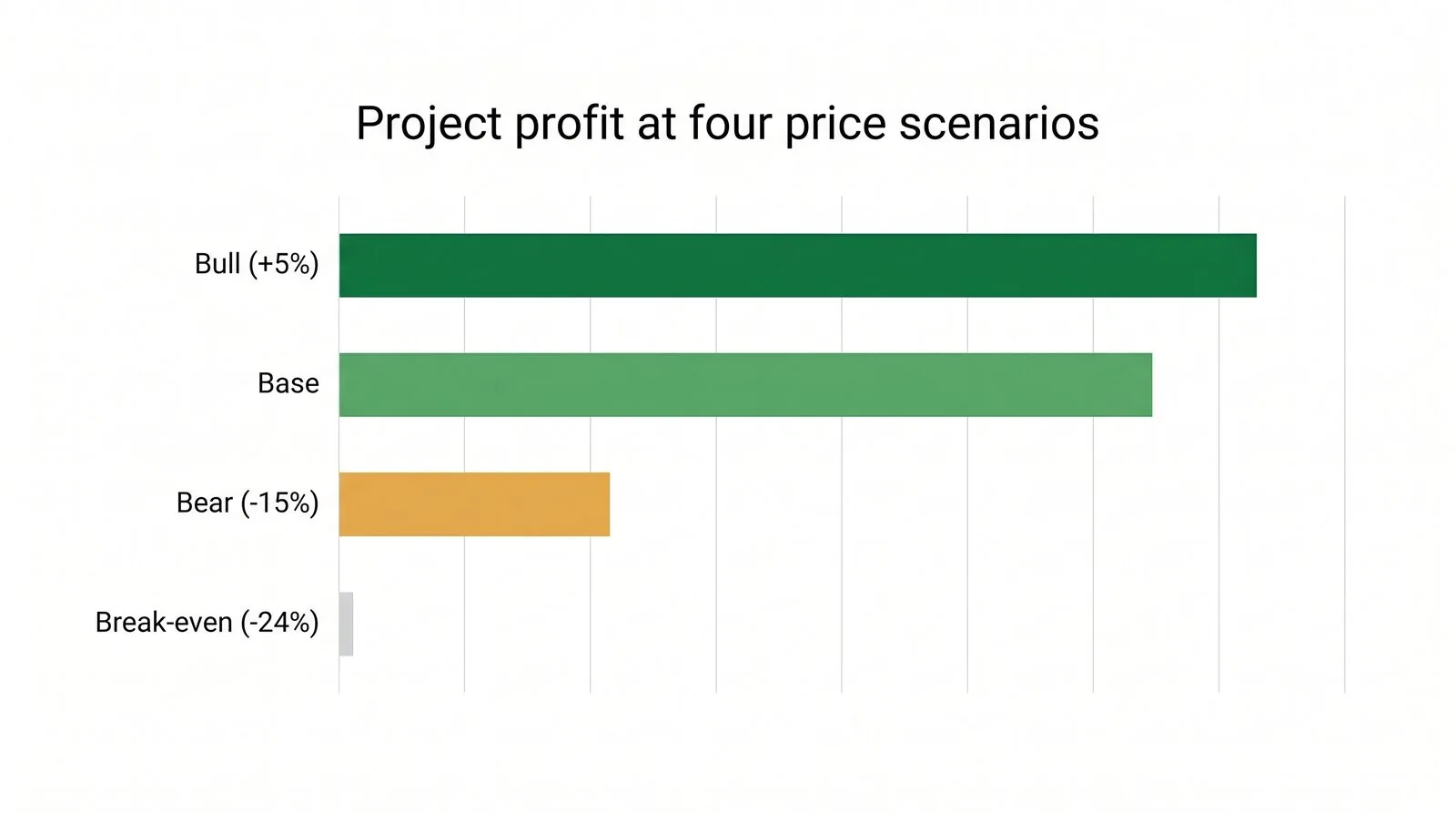

A 1.59x is the kind of number a careful person should be suspicious of. So here’s the part most pitches leave out — the floor.

This project breaks even at $976 per square foot for a nice Vancouver West property. It’s priced off comparable sales averaging $1,282, and the lowest comp in the data set is $1,118. Sale prices would have to fall roughly 24% — below anything currently transacting in that neighbourhood — before the project earns zero. Run the explicit bear case at prices down 15%, and it still produces about $849,000 in profit. And the 9% preferred return is the first money paid after the loan and capital are returned, so it sits in front of the part of the stack a soft market eats into first.

One more thing about that floor: the underwriting still carries a $116,454 density bonus charge. For a deal permitted after June 30, that charge is set to shrink — so the real floor is likely better than the one shown above.

The clock that actually applies

Two things converge on June 30. Province-wide, it’s the date the small-scale housing rules fully lock in, and the Province has shown it will enforce them. It overrode a resistant West Vancouver neighbourhood by Order in Council in April. And in Vancouver specifically, Council voted on May 5 to strip density bonus contributions for permits issued on or after that date. A West Side R1-1 deal acquired now would be permitted into the new, cheaper framework.

But the real clock on a lot like this isn’t a date. It’s absorption. A 10-of-10 lot doesn’t sit while organized capital is actively raising to buy exactly this. The best addresses are finite, and that’s the whole reason the arbitrage isn’t permanent.

How I’m thinking about it

If a deal only works when everything goes right, is it a deal or a bet dressed as one? This one breaks even 24% below market.

If you’ve believed the thesis for nine months and earned nothing from it, what is the belief worth until it becomes a position?

And when one of these clears our screen, what’s the actual difference between you and the investor who moves on it — other than being ready?

I’m asking these of myself too.

I don’t hold this lot. It’s public; you could go find it yourself. But finding it was never the work. Knowing it scores a 10, pricing the build, and structuring the capital so the floor sits 24% below market is the work. The next time a deal like this one clears our screen and we move to secure it, the only question that matters is whether you’re ready. If you want a first look when we do, just reply and I’ll put you on the short list. Replying commits you to nothing, and nothing here is an offer.

From the field this week

The example above is a real, currently-listed West Side property. I ran it through PlexRank to show the mechanics, not because we’ve tied it up. We’re also watching organized capital move in: a Vancouver competitor recently structured a multi-fund raise against an $87M project pipeline. That’s not a threat. It’s confirmation the window is real, and that the best lots are starting to get spoken for.

More next Saturday.

— David Babakaiff Co-Founder and CEO, VanPlex

You’re receiving this because you self-identified as an accredited investor on vanplex.ca and signed a Non-Disclosure Agreement. This communication is private and not intended for redistribution.